Chagee Holdings (CHA) IPO: Valuation Analysis and Low Float Volatility Potential

The TickerTrends Social Arbitrage Hedge Fund is currently accepting capital. If you are interested in learning more send us an email admin@tickertrends.io.

Check out our deep dive on Chagee ($CHA) here if you haven’t already:

Chagee Holdings Limited is set to make its public debut on the Nasdaq Global Select Market under the ticker symbol "CHA". The initial public offering consists of 14,683,991 American Depositary Shares (ADSs), with each ADS representing one Class A ordinary share of the company. The underwriters have an option to purchase up to an additional 2,202,598 Class A ordinary shares (represented by ADSs) within 30 days to cover over-allotments.

The expected price range for the IPO is set between US$26.00 and US$28.00 per ADS. Based on this range, Chagee aims to raise approximately $382 million to $411 million through the base offering, potentially increasing to around $440 million to $473 million if the over-allotment option is fully exercised. At the midpoint price of $27.00 per ADS, and considering the total expected outstanding shares post-IPO (183,549,892 shares, assuming no exercise of the over-allotment option), the implied market capitalization is approximately $4.96 billion. This aligns with reports suggesting a targeted valuation of up to $5.1 billion at the upper end of the price range.

The company employs a dual-class share structure. Upon completion of the offering (assuming no over-allotment exercise), there will be approximately 118,275,785 Class A ordinary shares and 65,274,107 Class B ordinary shares outstanding. Holders of Class A shares are entitled to one vote per share, while holders of Class B shares possess significantly enhanced voting power with ten votes per share. Both classes vote together on most matters. Crucially, founder and CEO Junjie Zhang is expected to hold shares conferring approximately 89% of the total voting power immediately following the IPO. Class B shares automatically convert to Class A shares upon transfer under certain conditions, whereas Class A shares are not convertible into Class B shares. This concentration of voting power effectively limits the influence of public shareholders on corporate governance matters.

A positive feature of the Chagee IPO is the substantial interest from cornerstone investors. Four independent institutional investors – identified as funds affiliated with CDH Investment Management, RWC Asset Management/Advisors, Allianz Global Investors Asia Pacific, and ORIX Asia Asset Management – have indicated non-binding interest in purchasing an aggregate of up to US$205.0 million worth of ADSs at the IPO price. This represents approximately 50% of the base offering size (at the midpoint price). Cornerstone investments are a common feature in Asian IPOs, particularly in Hong Kong, where they are seen as a mechanism to signal confidence in the offering, validate the valuation, and reduce underwriting risk, especially in volatile markets. While the specific lock-up terms for these US IPO cornerstones have not been released, generally such investors agree to hold their shares for a six month period after the IPO. The commitment from investors taking a significant portion of the deal further restricts the already limited supply of shares available for public trading in the initial months, which has the potential to amplify price volatility and aggressive price movement.

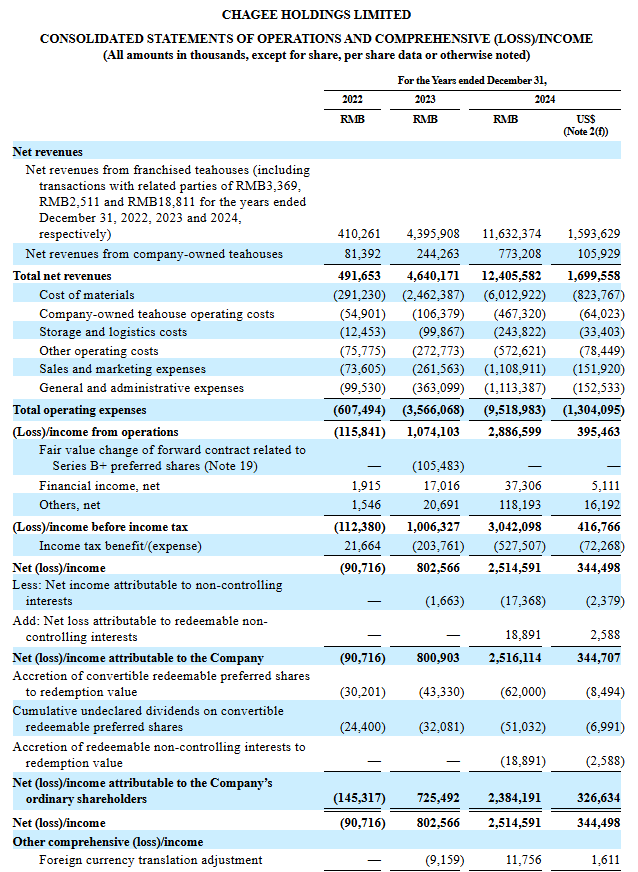

Financial Analysis:

Chagee Holdings has demonstrated extraordinary financial growth in recent years, largely mirroring its aggressive store expansion strategy. The company's revenue trajectory has been explosive, surging from RMB 492 million (approximately USD $68 million) in 2022 to RMB 12.41 billion (approximately USD $1.7 billion) in 2024. This represents a more than 20-fold increase over two years, with a year-over-year growth rate of 167.4% recorded in 2024 alone.

This top-line growth has translated into impressive profitability. After achieving its first annual profit of RMB 803 million in 2023, Chagee saw its net income more than triple in 2024 to RMB 2.51 billion (approximately USD $350 million). The company has also shown improving operational efficiency as it scales; the cost of materials as a percentage of total revenue decreased from 59.2% in 2022 to 48.4% in 2024, contributing to a strong net income margin of approximately 20% in 2024. This margin compares favorably to established players like Starbucks. Furthermore, the business generated positive free cash flow and maintained a healthy working capital surplus, indicating financial resilience alongside its rapid growth. Gross Merchandise Value (GMV), a key metric reflecting the total sales value across its network, also saw remarkable growth, reaching RMB 29.5 billion (USD $4.1 billion) in 2024, a 173% increase from the previous year.

However, beneath these impressive headline numbers, a concerning trend has emerged in the latter half of 2024 regarding same-store performance. While Chagee experienced very strong same-store GMV growth from the first quarter of 2023 through the second quarter of 2024 (consistently exceeding 35% year-over-year and peaking at 156.9% in Q4 2023), this momentum decelerated sharply later in the year. The company's year-over-year same-store GMV growth slowed to just 1.5% in the third quarter of 2024, and turned negative in the fourth quarter, recording an 18.4% decline. Chagee attributes this slowdown to demand being better fulfilled as store density increased, leading to a "normalized growth trajectory".

This deceleration in same-store growth is a significant development. While the full-year 2024 results are boosted by the sheer number of new store openings, the declining performance of existing stores raises questions about market saturation, intensifying competition, or potentially waning novelty appeal for its core products. This could mean that the phase of hyper-growth might be maturing, potentially leading to a more moderate future growth path than historical figures would imply.

Furthermore, the impressive 20% net margin achieved in 2024 occurred during this period of peak expansion. Sustaining such margins could prove difficult if same-store sales continue to lag, especially given the need for continued significant marketing investment to maintain brand visibility and the substantial costs associated with planned international expansion. The interplay between potentially slowing organic growth and ongoing investment requirements poses a challenge to maintaining the high profitability levels seen in 2024.

Valuation:

Based on its 2024 financial results (Revenue ~$1.7B, Net Income ~$350M), this midpoint valuation translates to:

Price-to-Sales (P/S) Ratio: $4.96B / $1.7B ≈ 2.9x

Price-to-Earnings (P/E) Ratio: $4.96B / $0.35B ≈ 14.2x

Peers Valuations:

Mixue Group (HKG:2097): Trades at significantly higher multiples, with a P/S around 6.0x and a P/E around 35x. Mixue focuses on the mass market with a much larger store network.

Guming Holdings (HKG:1364): Also commands higher multiples, with a P/S around 4.5x and a P/E around 25x. Guming operates in the mid-priced segment.

Starbucks (NASDAQ:SBUX): Trades at a P/S ratio of approximately 2.6x. While a mature global coffee giant, its P/S multiple provides a relevant comparison point in the premium beverage space.

Dutch Bros (NYSE:BROS): A rapidly expanding US drive-thru coffee chain, trades at significantly higher multiples, reflecting its growth trajectory, with a P/S ratio around 5.5x and a forward P/E ratio around 100x.

Compared to the close peers, Chagee's valuation is relatively conservative potentially due to geopolitical risks and market conditions. Additionally, the macro risks like US-China trade tensions and potential delisting of Chinese stocks could mute demand. The slowdown in same-store growth is also concerning and should be monitored closely.

The Low Float Factor

Chagee Holdings IPO could see a substantial surge due to its exceptionally low public float. The public float refers to the number of a company's shares that are available for trading by the general public on the open market, excluding shares held by insiders (like executives and large strategic holders) and restricted shares not yet eligible for sale. Based on the offering structure, Chagee is making 14,683,991 ADSs available to the public out of a total of 183,549,892 outstanding ordinary shares immediately post-IPO (assuming no exercise of the underwriters' over-allotment option). This results in a public float percentage of approximately 8.00%. The low float could lead to heightened potential for stock price volatility. With a smaller pool of shares available, even moderate buy or sell orders can have a disproportionately large impact on the stock price.

The impact of this low float could be intensified by the significant cornerstone investment. Cornerstone investors are expected to take up approximately half of the offered ADSs. Assuming these investors are subject to typical post-IPO lock-up agreements (often six months or longer), the effective number of shares freely trading in the market immediately after the IPO and for the duration of the lock-up period will be even smaller than the headline 8.00% figure – potentially less than 4% of total outstanding shares.

Case Study: WeBull's (BULL) Post-SPAC Surge

The market debut of WeBull provides a compelling case study on the potential impact of low-float dynamics. WeBull, a digital investment platform popular among retail traders, completed its business combination with the Special Purpose Acquisition Company (SPAC) SK Growth Opportunities Corporation (formerly SKGR) on April 10, 2025. The combined entity began trading on the Nasdaq on April 11, 2025, under the ticker symbol "BULL" for its ordinary shares, alongside warrants trading as "BULLW" and "BULLZ". The deal targeted an enterprise value of approximately $7.3 billion.

SPAC transactions often lead to low public floats. This occurs because SPAC shareholders are typically given the option to redeem their shares for cash (usually around the initial $10 IPO price plus interest) just before the merger closes. In recent years, particularly as market sentiment towards SPACs cooled, redemption rates have often been very high (sometimes exceeding 90%), leaving only a small percentage of the original SPAC shares in the hands of public investors post-merger. Immediately following its Nasdaq listing, WeBull's stock (BULL) experienced extraordinary volatility with the stock price surging dramatically in the session. The stock climbed over 500%, reaching intraday highs ~$80.

This explosive price action is largely attributable to the low-float conditions characteristic of many de-SPACs. The limited supply of publicly traded shares, combined with speculative interest likely amplified by WeBull's existing brand recognition within the retail trading community, created a technical setup ripe for a rapid price increase. The surge appeared driven more by these technical supply/demand dynamics than by immediate fundamental news following the merger completion.

Case Study: Newsmax's (NMAX) Explosive IPO Debut

Newsmax, Inc., the conservative media company, also provides a great case study in extreme IPO volatility potentially linked to initial share supply dynamics. Newsmax went public via a traditional IPO on the New York Stock Exchange (NYSE) under the ticker "NMAX”. The IPO was priced at $10.00 per share, with the company selling 7.5 million shares of its Class B Common Stock.

The stock's debut was nothing short of spectacular. On its first day of trading, NMAX shares surged more than 700%, closing the session at $82.25. This dramatic rise gave the company an immediate market capitalization exceeding $10 billion on paper.

Analyzing the float situation requires careful interpretation. While the initial offering consisted of only 7.5 million shares, later financial data sources reported a much larger public float of 64.84 million shares, representing about 73% of the 89.17 million total outstanding shares. This discrepancy highlights a crucial point: the initially available float on day one can be significantly different from the float reported later, after lock-up periods expire or secondary shares become available. The extreme first-day price surge strongly suggests that the market was reacting to the scarcity of the initial 7.5 million shares being offered, rather than the larger eventual float. This limited initial supply, when met with high demand, likely created the conditions for the massive price spike.

The drivers behind this surge was the severely limited initial share supply creating a technical bottleneck. This was likely amplified by Newsmax's high brand recognition (though polarizing), attracting significant speculative interest from traders looking to capitalize on the low-float dynamics. The company's underlying financials at the time (reporting widening losses despite revenue growth) seemed secondary to the technical and sentiment-driven trading activity on its debut day. Restricting the initial supply, even if the eventual float is larger, can mimic the volatility effects typically associated with structurally low-float stocks. Furthermore, the case suggests that strong brand recognition, even if controversial, can act as an accelerant, drawing in retail and speculative interest that magnifies the price impact of a limited initial share supply.

Chagee's Debut: Potential for A Surge?

Chagee Holdings' upcoming IPO could present a high potential for initial trading volatility. The company boasts a compelling narrative of rapid historical growth and strong profitability in 2024, coupled with ambitious global expansion plans. However, this is tempered by concerning signs of slowing same-store growth momentum and the inherent risks associated with operating significantly in China. Its IPO valuation, while appearing somewhat discounted relative to high-flying Hong Kong peers like Mixue and Guming, still carries expectations that might be challenged if growth normalizes faster than anticipated. The offering is significantly de-risked by substantial cornerstone investor commitments, covering roughly half the deal.

The critical factor, however, is the exceptionally low public float. At approximately 8.00% of total outstanding shares, and potentially less than 4% effectively tradable at launch due to cornerstone lock-ups, Chagee presents an extreme case of limited share supply. This technical setup bears striking resemblance to the conditions preceding the volatile debuts of WeBull (BULL) and Newsmax (NMAX). Like WeBull, which emerged from a de-SPAC process, Chagee has a restricted number of shares available for public trading. Like Newsmax, whose IPO surge was driven by the limited number of shares initially offered, Chagee's effective float available to non-cornerstone investors is minimal at the outset. Chagee also possesses growing brand recognition within its sector, potentially attracting speculative interest similar to WeBull and Newsmax.

Chagee's IPO thus presents a scenario where potent technical factors (low float) could clash with emerging fundamental questions (slowing growth, risks). The initial trading phase is highly likely to be dominated by technical scarcity, potentially leading to significant price swings reminiscent of WeBull and Newsmax. However, the sustainability of any initial price surge will ultimately depend on whether the company can address growth concerns and whether its ongoing performance justifies its valuation in the face of market and geopolitical headwinds. The presence of large cornerstone investors might influence post-lockup dynamics but is unlikely to prevent initial volatility driven by the remaining, extremely small, freely tradable float.

Investors considering participation, especially in early trading, must be acutely aware of the heightened risks. The low float structure makes CHA susceptible to extreme price fluctuations, potentially disconnecting it from fundamental value in the short term. Liquidity could also be a challenge, making it difficult to enter or exit large positions without impacting the price. Long-term success will hinge on Chagee's ability to navigate the competitive landscape, manage its franchise network effectively, successfully expand internationally, and mitigate the various operational and geopolitical risks outlined in its filings.

Conclusion:

The upcoming IPO of Chagee Holdings Limited (CHA) presents a multifaceted investment case, dominated by a history of hyper-growth juxtaposed against recent signs of moderation and significant structural factors related to its offering. The company has successfully scaled its premium tea beverage concept at an astonishing pace, achieving substantial revenue and profitability, particularly in 2024. Its franchise-led model has proven effective for rapid expansion, though it carries inherent dependencies and risks.

From a valuation standpoint, the IPO appears priced below its most successful Hong Kong-listed Chinese peers, potentially reflecting US market caution, geopolitical considerations, or concerns about the sustainability of its growth trajectory, particularly the notable slowdown in same-store GMV in late 2024. The poor post-IPO performance of other listed tea chains like Nayuki and ChaPanda serves as a cautionary tale regarding market sentiment in this competitive sector.

However, the most defining characteristic of the Chagee IPO is its extremely low public float, estimated at just 8.00% of total shares, and effectively even lower in the initial trading period due to the large, locked-up cornerstone investor tranche. This technical setup is the "wildcard" factor. As demonstrated by the recent volatile debuts of WeBull and Newsmax, limited share supply can fuel dramatic price surges in the short term, often driven by speculative interest capitalizing on scarcity.

Therefore, Chagee's stock (CHA) is highly susceptible to significant price volatility immediately following its listing. The technical factors favoring such volatility are strong. Investors considering trading CHA in the early stages must be prepared for potentially extreme price swings, both upward and downward, and acknowledge the associated liquidity risks. While the potential for rapid gains exists, mirroring the WeBull and Newsmax examples, the risk of sharp reversals is equally significant, especially if market sentiment shifts or fundamental concerns come to the forefront.

Ultimately, the long-term investment merit of Chagee will depend not on initial trading dynamics, but on its ability to successfully transition from hyper-growth to sustainable, profitable expansion, manage its extensive franchise network, navigate the intense competition in the beverage industry, and mitigate the operational and geopolitical risks inherent in its business model and China-centric operations. The low float may ignite initial fireworks, but fundamentals will dictate the enduring value.