$EAT Brinker International Earnings Preview | TickerTrends.io

$EAT KPI Metrics, Earnings Preview Tracking, Expectations And Alternative Data Comps

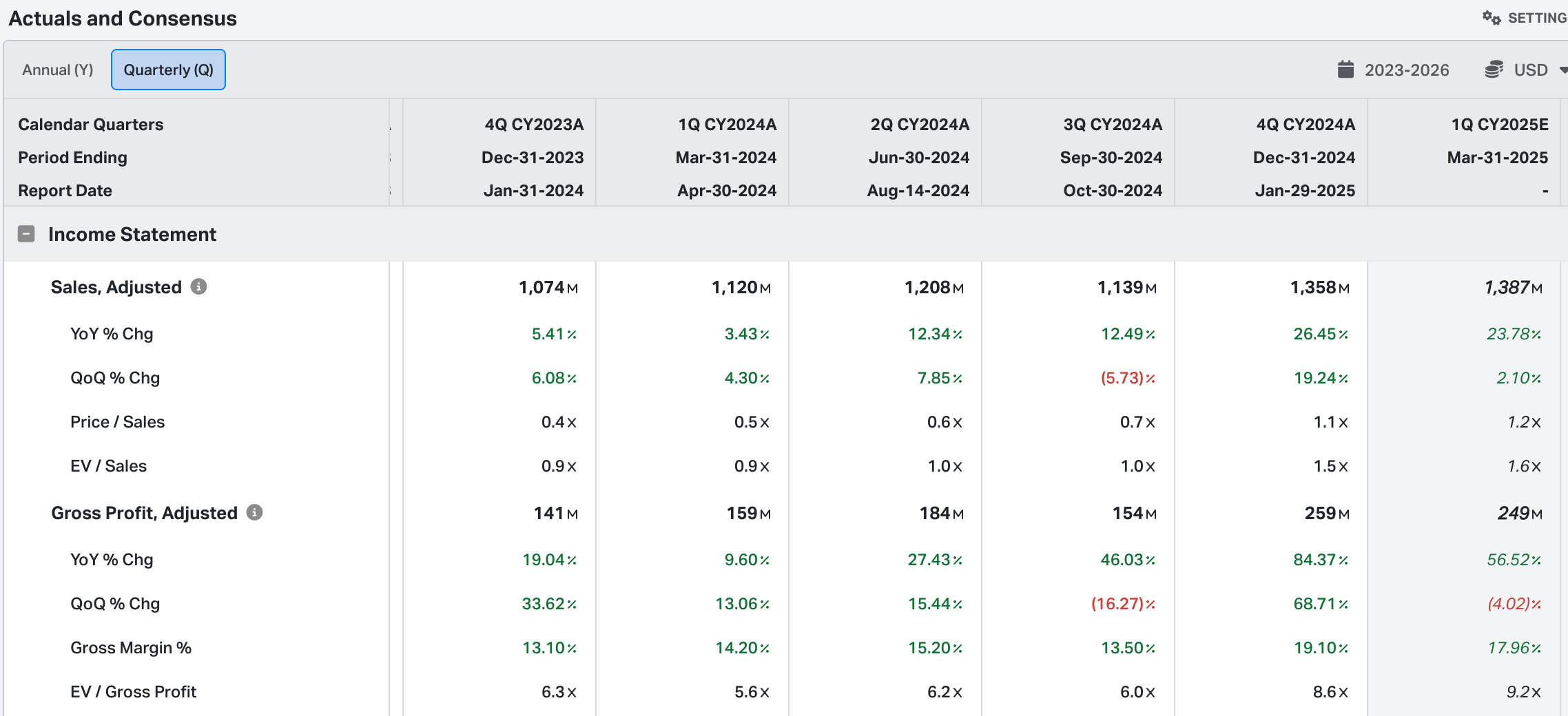

Market Expectations

Analysts expect 23.78% YOY growth which is an acceleration of 2.10% QoQ going into Q1 2025.

Brinker International reported robust financial results for the second quarter of fiscal 2025, ending December 25, 2024, driven primarily by exceptional performance at its flagship brand, Chili’s. GuruFocus

Financial Highlights

Total Revenues: $1.36 billion, a 26% increase from $1.07 billion in Q2 FY24.

Company Sales: $1.35 billion, up from $1.06 billion year-over-year.

Operating Income: $156.0 million, with an operating income margin of 11.5%, nearly doubling from 5.8% in the prior year.

Restaurant Operating Margin (non-GAAP): 19.1%, compared to 13.1% in Q2 FY24.

Net Income: $118.5 million, up from $42.1 million in the same quarter last year.

Diluted EPS: $2.61, compared to $0.94 in Q2 FY24.

Adjusted EPS (excluding special items): $2.80, up from $0.99 in the prior year. PR Newswire

Segment Performance

Chili’s Grill & Bar:

Comparable restaurant sales surged by 31.4%, driven by a 19.9% increase in traffic.

Sales growth was fueled by strategic advertising campaigns, including the "Better Than Fast Food" initiative, and operational enhancements that improved the guest experience.

The Triple Dipper promotion accounted for 14% of total sales, doubling its share from the previous year.

Restaurant operating margin (non-GAAP) improved to 18.7%, up from 11.6% in Q2 FY24. GuruFocus Nasdaq Restaurant Dive PR Newswire

Maggiano’s Little Italy:

Comparable restaurant sales increased by 1.8%, primarily due to menu pricing strategies.

Restaurant operating margin (non-GAAP) remained strong at 22.7%, slightly down from 22.9% in Q2 FY24. Brinker Investors PR Newswire

Operational and Strategic Developments

Brinker completed the installation of new kitchen display systems and began deploying TurboChef ovens across all Chili’s locations, enhancing kitchen efficiency and consistency.

The company streamlined operations by removing the dedicated "It’s Just Wings" station, reallocating resources to high-performing menu items.

General and administrative expenses increased due to higher incentive compensation and investments in technology initiatives. Nasdaq GuruFocus

Fiscal 2025 Outlook

Brinker International updated its fiscal 2025 guidance as follows:

Total Revenues: Expected to be between $5.15 billion and $5.25 billion, up from the previous estimate of $4.70 billion to $4.75 billion.

Adjusted EPS (excluding special items): Projected to range from $7.50 to $8.00, an increase from the prior estimate of $5.20 to $5.50.

Capital Expenditures: Anticipated to be between $240 million and $260 million. investopedia.com Nasdaq PR Newswire

Alternative Data

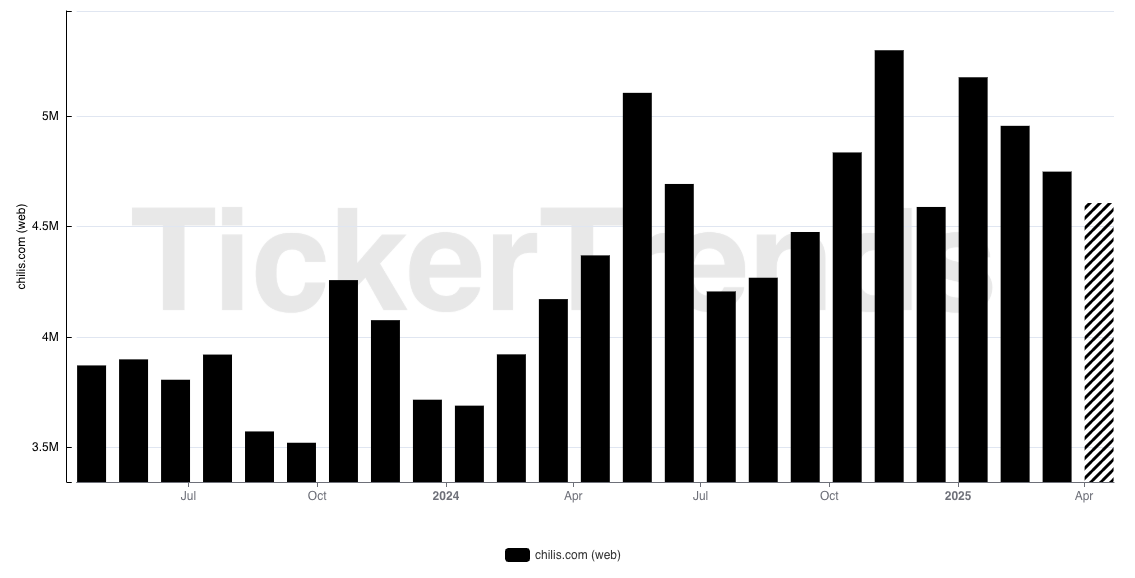

Web Traffic

Recent data indicates a -3.00% MoM slowdown in web traffic.

Search Trends

Recent data indicates a +22.23% YoY acceleration in search trends.

Mobile Data

Recent data indicates a -1.20% MoM slowdown in android mobile app usage.

Recent data indicates a -2.87% MoM slowdown in ios mobile app usage.

Social Data

Recent data indicates a +22.99% MoM acceleration in social following.

Wiki

Recent data indicates a -10.69% MoM slowdown in wikipedia searches.

Conclusion

Brinker International delivered a standout Q2 FY25, with Chili’s driving exceptional sales and margin expansion. Strategic promotions, operational improvements, and increased traffic helped power the company's significant outperformance on both revenue and earnings. The raised full-year guidance reflects strong internal confidence and momentum.

However, while the top-line and operating results are impressive, some alternative data signals introduce a more tempered view. Web and mobile engagement showed modest slowdowns month-over-month, and Wikipedia interest declined, hinting at potential plateauing in brand curiosity. As Brinker’s story gains more attention from the Street, expectations are rising quickly—and the company will need to continue executing flawlessly to justify the heightened outlook.

Overall, while the core business appears healthy and well-managed, investors should remain attentive to the sustainability of recent traffic gains and whether broader consumer enthusiasm keeps pace. Alternative data signals remain supportive—but slightly more mixed—suggesting it may be time to watch for consistency, not just acceleration.

Track real-time alternative data on TickerTrends.io