Hidden Equity Upside in $GAIN: Schylling Position Driving Potential NAV Re-Rating

Strong NeeDoh demand and accelerating EBITDA growth could push NAV above $16/share, with embedded equity optionality alongside a stable yield profile

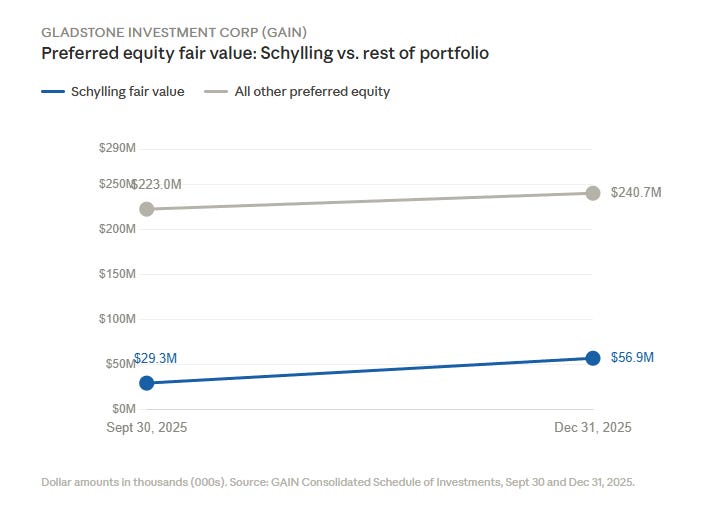

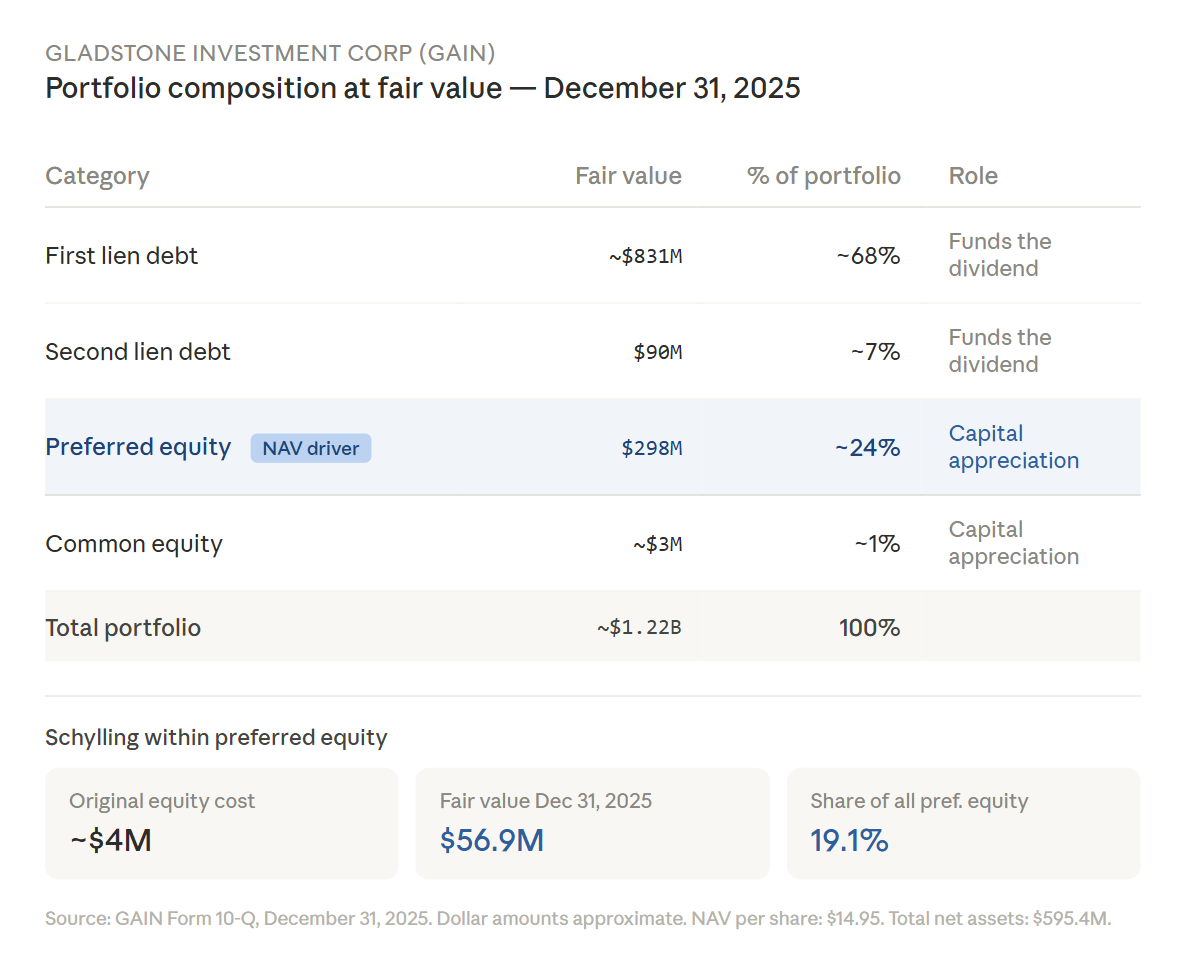

Gladstone Investment Corporation first invested in Schylling, Inc. in 2013 through a ~$20M buyout, structured primarily as debt with a ~$4M equity component. The debt was repaid over time, leaving a small equity stake that remained largely unchanged for years, until the recent growth driven by NeeDoh.

The ~$4M equity stake was valued at $29.3M as of September 30, 2025, and rose to $56.9M by December 31, 2025. Management noted this increase was entirely driven by EBITDA growth, not multiple expansion, highlighting a significant and largely unexpected NAV contributor for GAIN.

In fiscal Q3 2025 alone, Schylling’s valuation increase generated ~$27.7M in unrealized gains for GAIN, exceeding the contribution from the rest of its preferred equity portfolio and representing a meaningful per-share impact.

The Viral Moment: NeeDoh Sold Out Everywhere

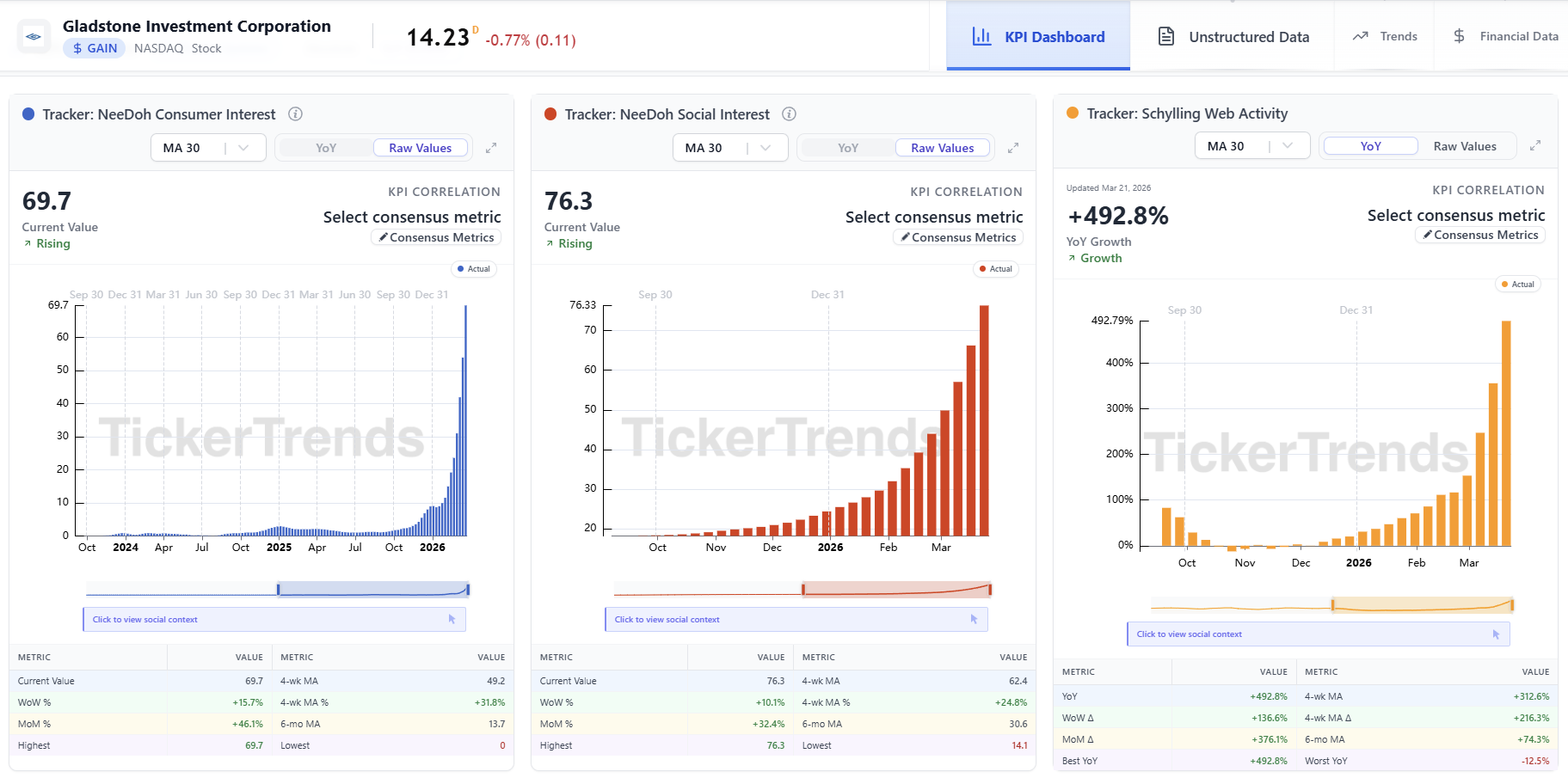

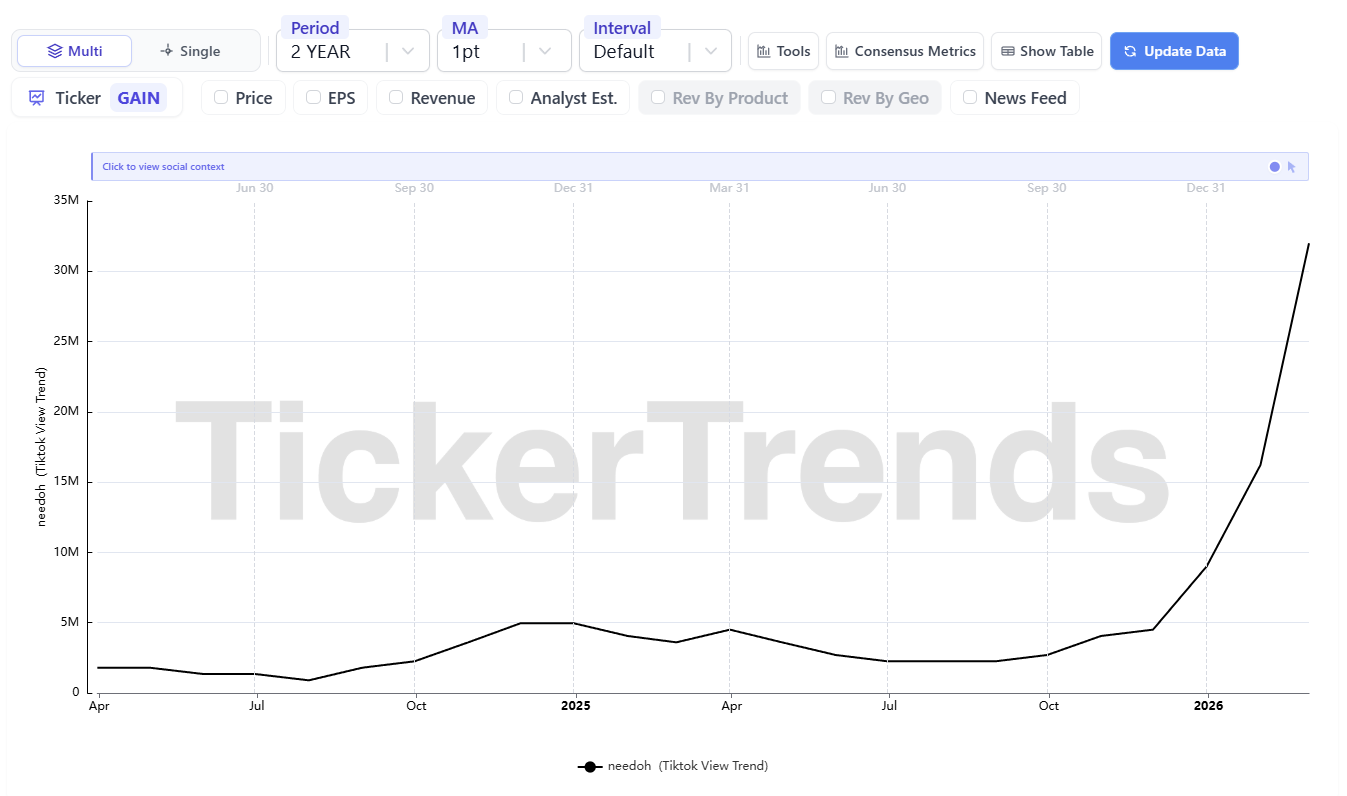

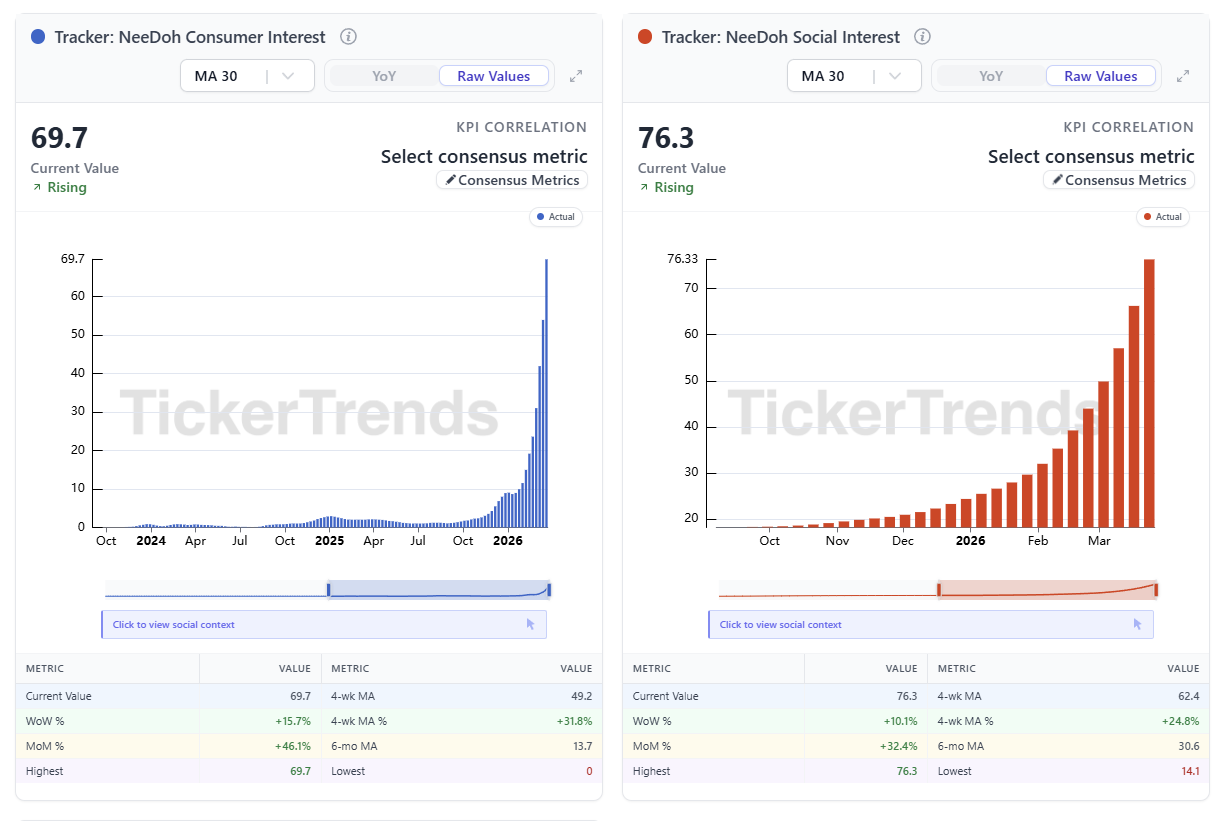

Our NeeDoh consumer interest tracker registered a roughly 4x increase during Q4 2025 alone, moving from approximately 2 to 8 on a normalized basis.

Since December 31, 2025, the last quarter-end date reflected in GAIN’s filings, our consumer interest tracker has risen an additional 8x, now registering 69.7. The next quarterly mark will be the first opportunity for the market to see whether the EBITDA trajectory has continued to follow the consumer data higher.

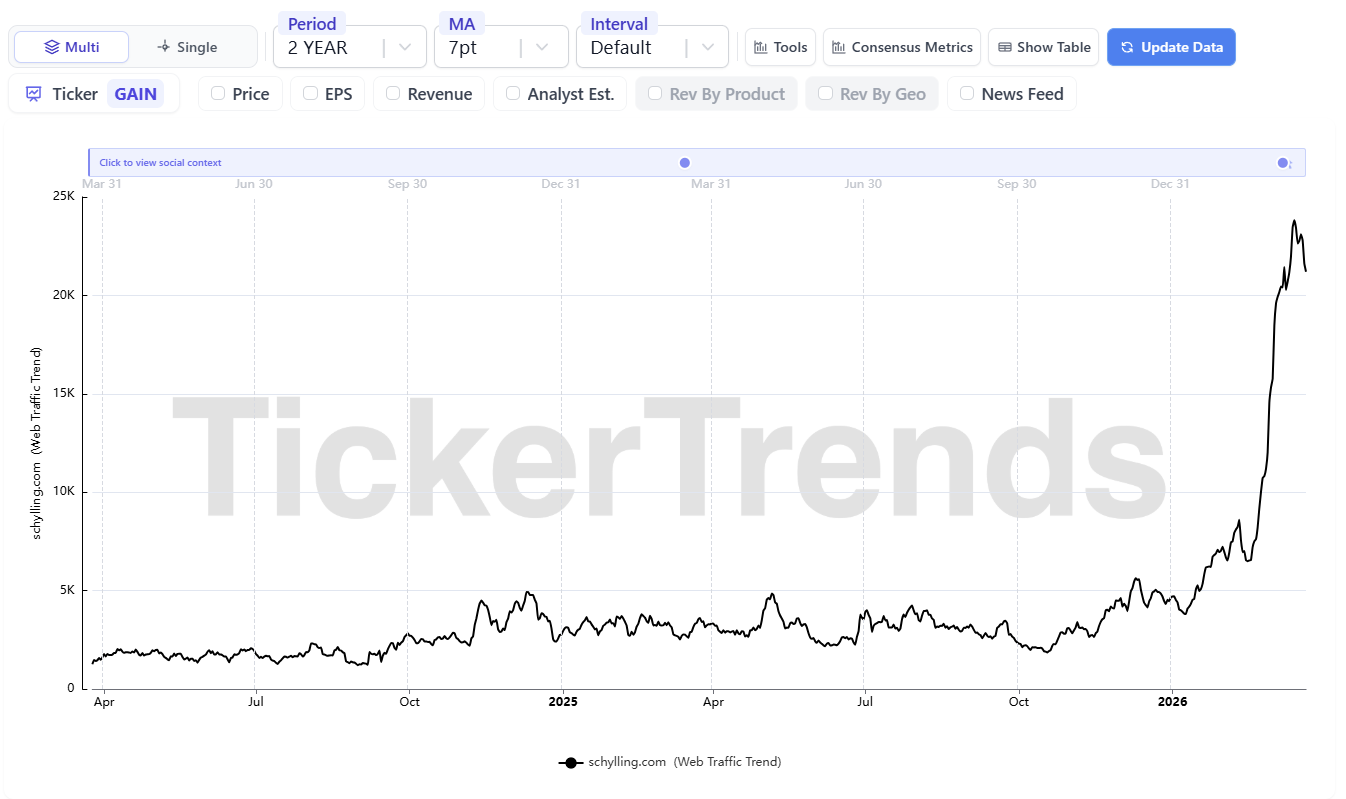

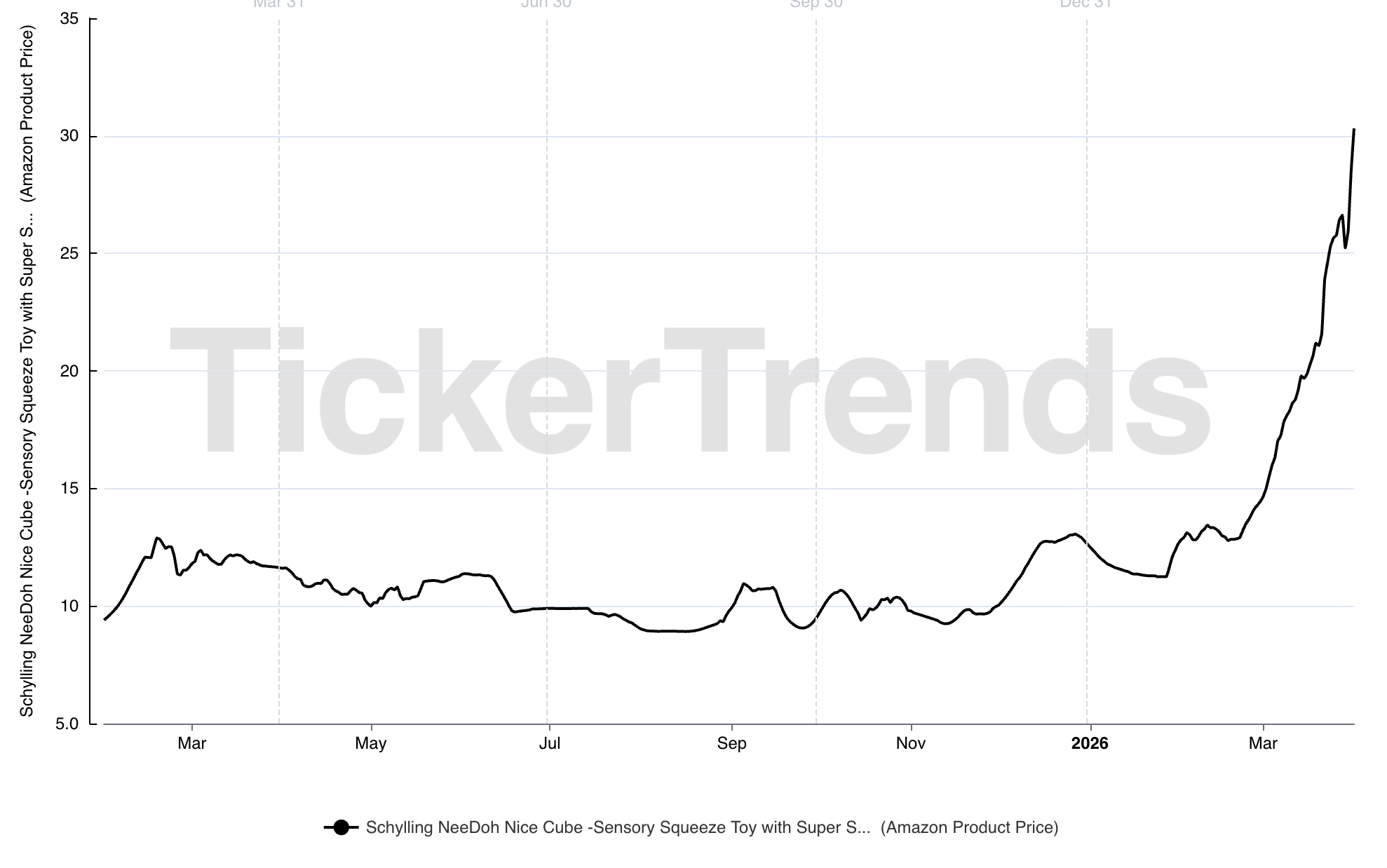

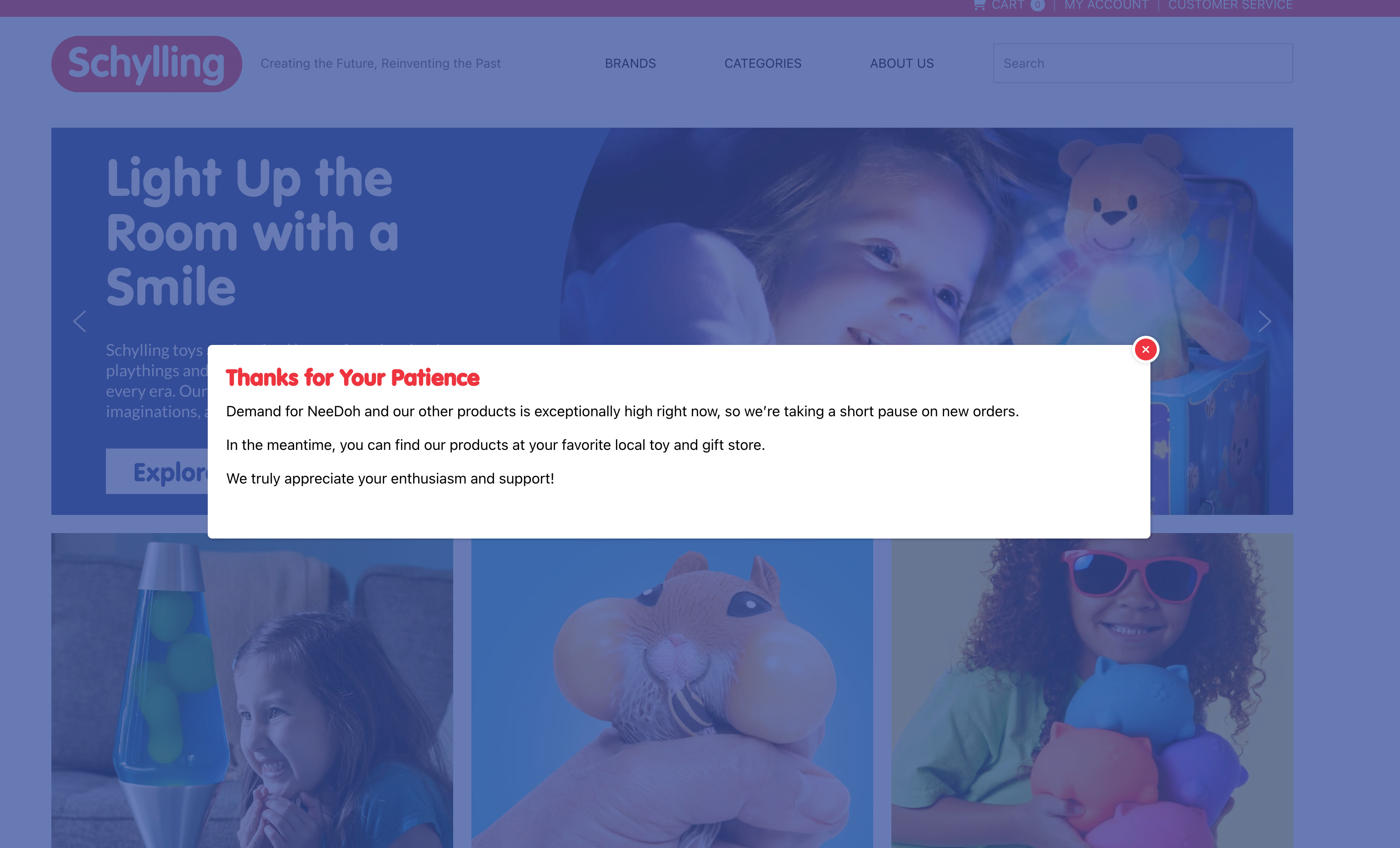

Website Traffic to “schylling.com” is 5x higher now versus the end of Q4 2025, up to 22k daily visits.

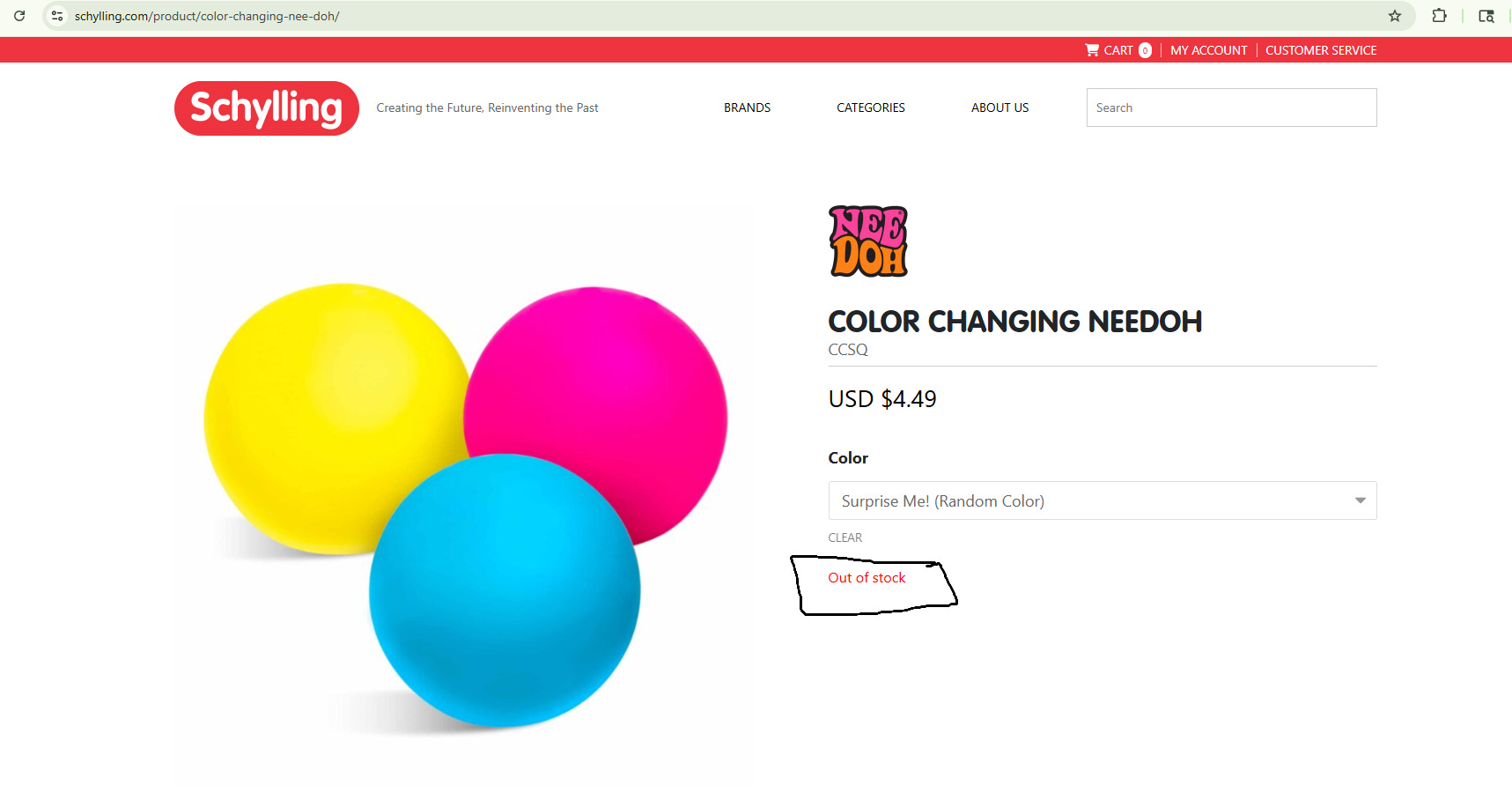

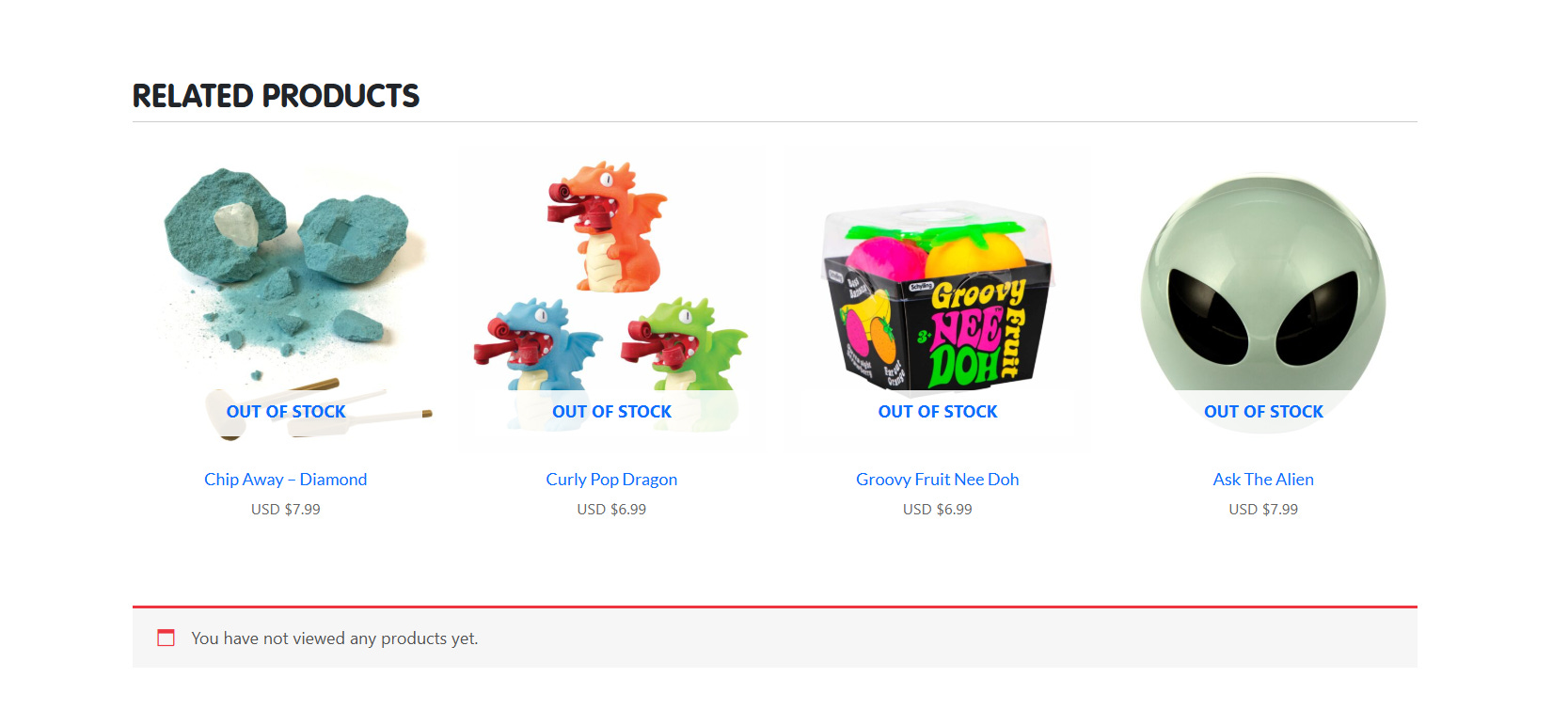

Almost all items are out of stock at the current moment, including, non-Nee Doh products.

TikTok, Amazon, and Google Search volume has skyrocketed for “needoh” over the quarter.

As of late March 2026, social media platforms are saturated with NeeDoh-related discussions, with consumers widely expressing frustration over the product’s limited availability.

Dedicated Reddit threads have emerged to track remaining inventory, and users are actively sharing real-time sightings of in-stock locations. Retailers have confirmed that this surge in demand exceeded Schylling’s expectations, resulting in widespread stockouts and an inability to adequately meet consumer demand.

What this means for GAIN

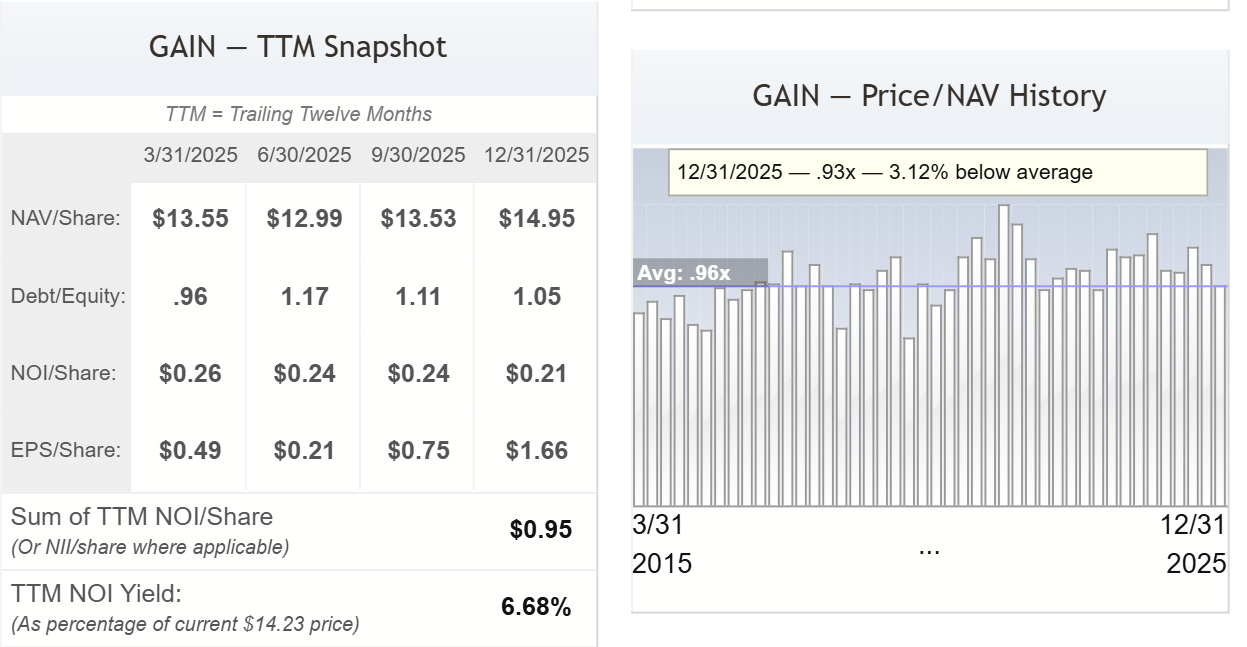

GAIN’s total net assets as of December 31, 2025 were roughly $591 million (NAV of $14.95 × approximately 39.5 million shares). The Schylling preferred stake alone, at $56.9 million fair value, represents roughly 9.6% of total NAV.

GAIN’s debt portfolio (~75% of assets) continues to generate stable monthly income, supporting its $0.08/share dividend. The key change is in the equity book: Schylling alone added ~$0.70/share to NAV in a single quarter (+$27.7M on 39.8M shares). Shares currently trade at a ~7% discount to the $14.95 NAV, in line with historical ranges (~±10%).

TickerTrends estimates Schylling’s preferred stake could increase from $56.9M to ~$110M, implying an additional ~$53.1M in unrealized gains (~$1.33/share), bringing NAV to ~$16.28. This assumes no net change across the remainder of the portfolio. Historically, non-Schylling NAV movements have been ~±$0.50/share.

Risks to Consider

Investors should weigh several risks:

Fad risk: Demand for NeeDoh may reverse quickly. Ongoing monitoring of consumer and social trend data on TickerTrends is critical.

Valuation opacity: Schylling is privately held, and fair value is determined by GAIN’s board using TEV-based methodologies. Underlying EBITDA is not independently verifiable, and marks may be conservative.

Credit risk: Despite predominantly first-lien exposure, deterioration in other portfolio assets could offset Schylling-driven NAV gains.

BDC structure: External management and incentive fees tied in part to unrealized gains create potential valuation conflicts.

Persistent discount to NAV: Even with NAV expansion (e.g., >$16/share), shares may continue to trade at a discount. The sector has faced pressure following recent credit events (e.g., Tricolor, First Brands Group).

Limited price reaction to unrealized gains: Prior earnings (Feb 3, 2026) saw only modest share price movement despite NAV appreciation, highlighting risk that future markups remain under-reflected.

Supply constraints: Rapid demand acceleration may have outpaced Schylling’s production capacity, potentially limiting realized revenue relative to observed demand signals.

Conclusion

Gladstone Investment Corporation holds a highly asymmetric equity position in Schylling. A $4M preferred investment has already been marked to $56.9M (Dec 31, 2025), driven by confirmed EBITDA growth. TickerTrends estimates a potential revaluation to >$110M in the upcoming May earnings.

Consumer and alternative data indicate continued strength in NeeDoh demand through Q1 2026. If EBITDA expansion tracks observed sell-through trends, NAV could exceed ~$16.30/share.

GAIN currently trades at ~7% below NAV, consistent with historical ranges. The setup offers a combination of stable yield and upside from embedded equity revaluation. Risk/reward appears favorable, though positioning requires close monitoring of underlying demand and KPI trends.