Kimi K3: The Next Major Open-Weight Model Release?

Early tester feedback suggests Moonshot could have another GLM-5.2-type moment, with 133.HK offering the only meaningful listed exposure.

Moonshot AI appears close to releasing Kimi K3, potentially its largest model upgrade to date.

GLM-5.2 was released in June with public weights and a 1 million-token context window. Its strength in coding and long-horizon agent tasks quickly drove attention outside China, with the model gaining usage on OpenRouter and being discussed as one of the first open-weight models that worked well as a general coding agent.

K3 has the potential to create a similar reaction. Early tester feedback has compared it with Fable-level models, while some individual Arena examples show it competing with or leading existing frontier models. The evidence remains selective, but the bar appears to be much higher than a normal incremental Kimi release.

For listed exposure, China Merchants China Direct Investments, or 133.HK, owns a meaningful Moonshot stake. The position gives the fund leverage to both K3 adoption and any resulting reset in Moonshot’s private-market valuation.

Kimi K3

Moonshot released a trailer for K3 on 16 July, but has not yet published a model card, official benchmarks, API pricing, weights or licensing terms. The Kimi API platform still lists K2.7 Code as its latest model, while Moonshot’s main site continues to feature K2.6.

Reported specifications include a roughly 2.5 trillion-parameter mixture-of-experts architecture and a context window of around 1 million tokens. These figures remain unconfirmed and appear to come from a small number of reports that have since been repeated across other outlets. Until Moonshot publishes official details, the architecture and parameter count should be treated as reported rather than confirmed.

The early outputs suggest K3 may be focused on long-horizon agent and coding tasks. This would put it directly against GLM-5.2, Opus and Fable in the areas currently driving the most developer interest: extended coding tasks, frontend generation and autonomous multi-step workflows.

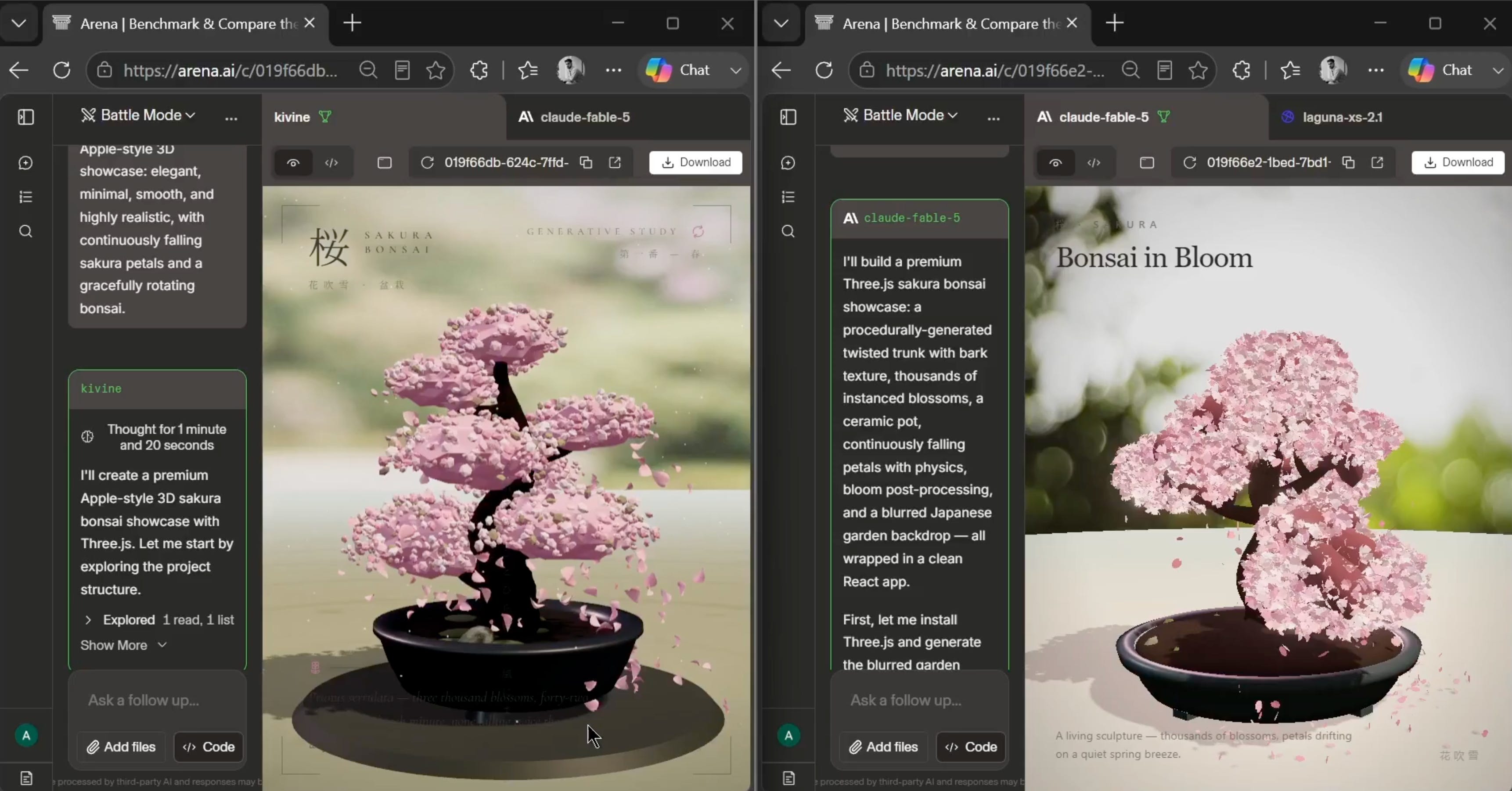

One early frontend test described K3’s output as among the best the tester had seen from the prompt, although it reportedly took 35 minutes to complete. In another Arena comparison, Fable 5 finished faster and was described as having cleaner controls, while K3 produced a broader result.

The early examples are positive but mixed. Some comparisons show K3 leading, while others still favor existing models. Without broader benchmarks, standardized testing and official pricing, it is worth being cautious around the pre-release hype.

Moonshot’s momentum into the release

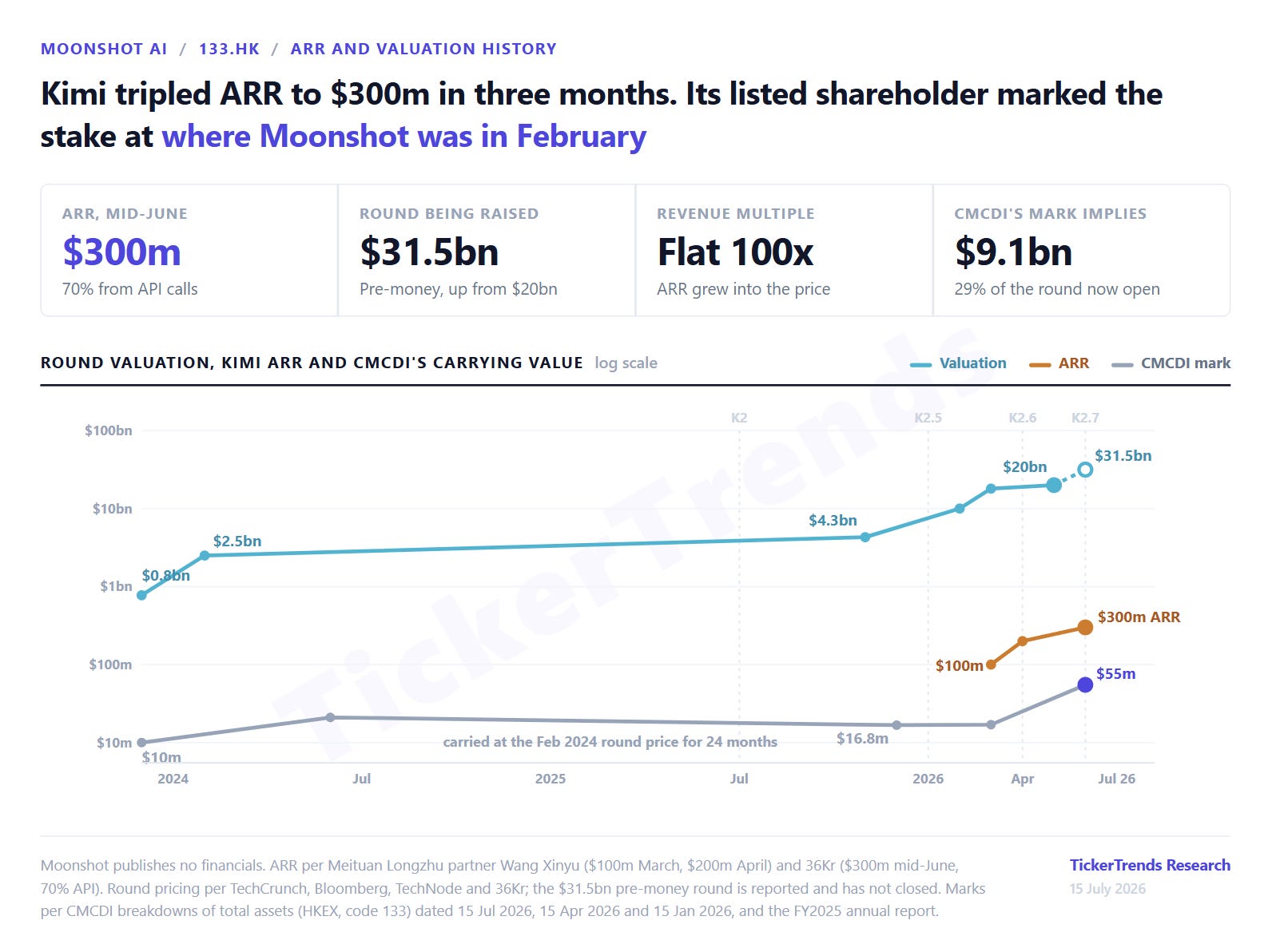

K3 is arriving as Moonshot’s commercial and developer momentum has already accelerated. Moonshot’s ARR reportedly moved from more than US$100 million in March to above US$200 million in April. Later reports put ARR above US$300 million by mid-June, with API revenue representing more than 70% of the total. The US$300 million figure comes from secondary reporting and has not been disclosed in Moonshot financial statements.

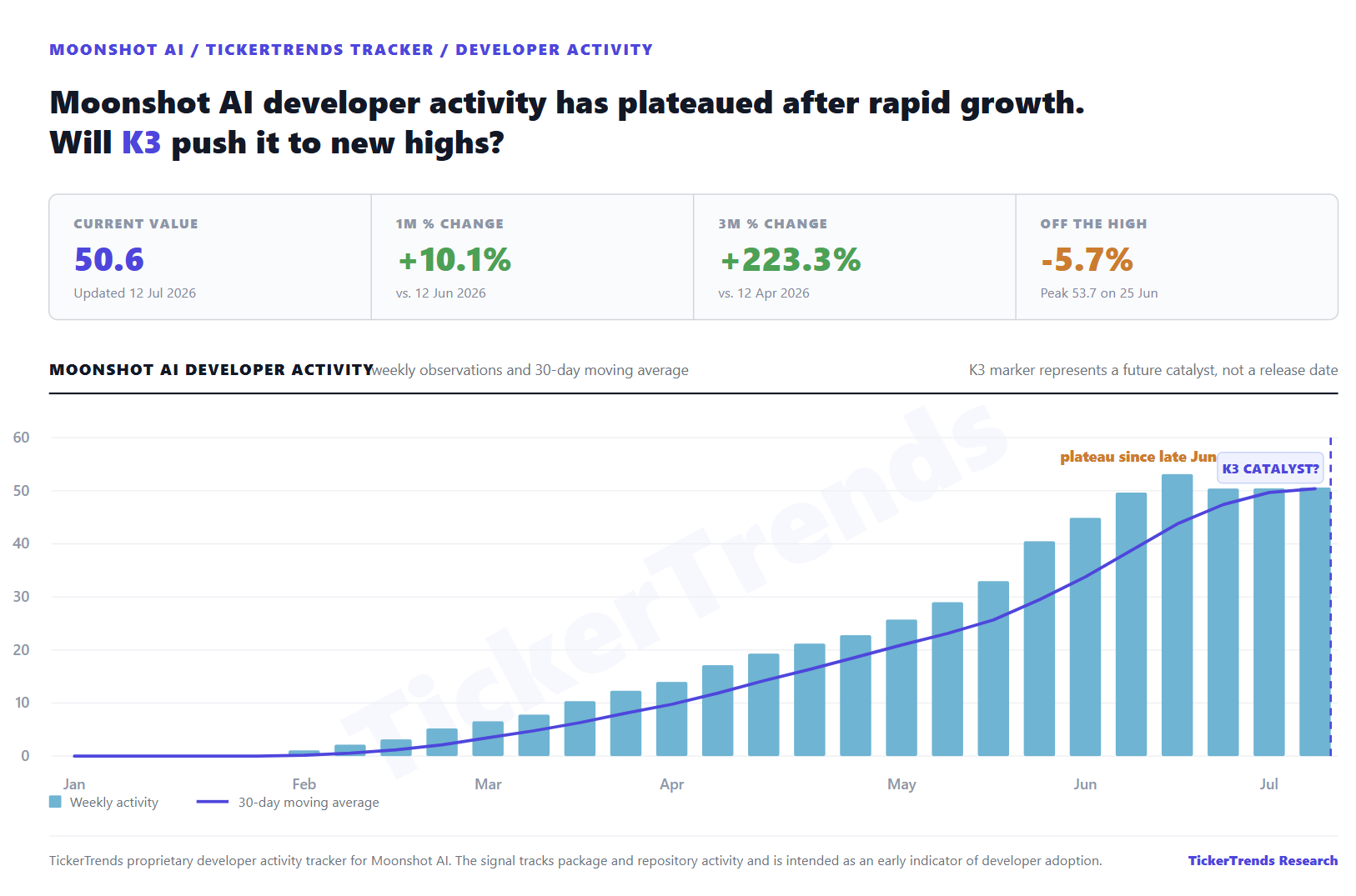

TickerTrends Developer Activity rose rapidly during this shift, increasing 223% over the past three months. Activity has since plateaued slightly below its late-June high, making K3 the next major potential catalyst.

The listed exposure

Moonshot is private, but 133.HK owns a direct stake through its participation in Moonshot’s December 2023 Series A. The fund initially invested US$10 million for a 1.29% interest, although subsequent rounds have diluted the position.

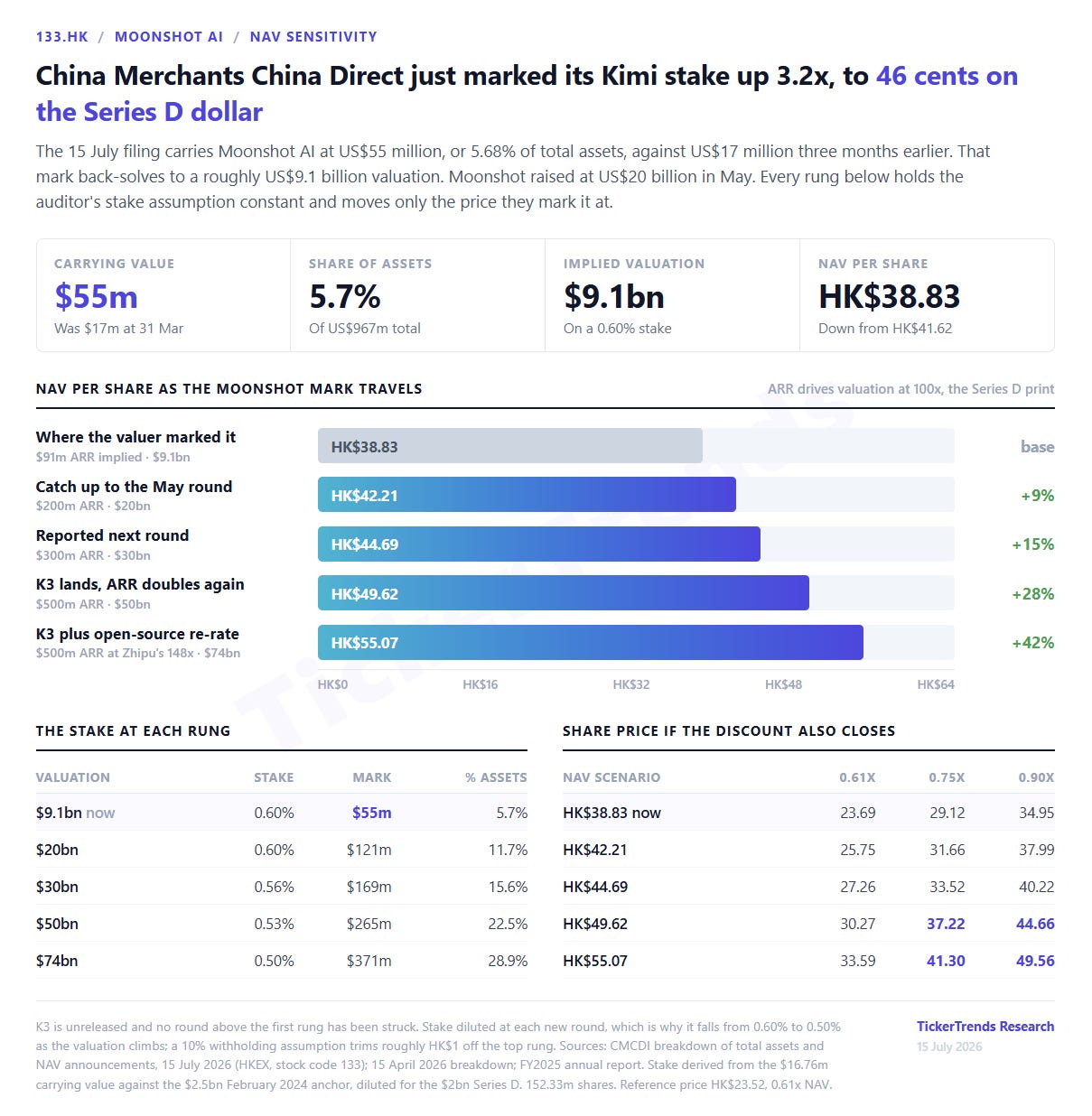

On 15 July, the fund published its asset breakdown as of 30 June and increased the Moonshot carrying value from US$17 million to US$55 million. Moonshot now represents 5.68% of the fund’s US$967 million of total assets, up from 1.67% at the end of March.

The US$55 million mark implies a Moonshot valuation of approximately US$9.1 billion based on the fund’s estimated 0.60% stake. That is broadly consistent with Moonshot’s early-2026 financing level but remains below the May round, when Moonshot raised approximately US$2 billion at a post-money valuation above US$20 billion. That round was led by Meituan’s investment arm.

Moonshot has since reportedly been seeking another round at around US$30 billion, with some reporting placing the proposed pre-money valuation at US$31.5 billion. The round remains under discussion, so that figure should not be treated as a completed valuation.

At the May round price, the position would be worth approximately US$121 million after allowing for dilution, or around 11.7% of the fund’s assets. At a US$30 billion valuation, the position would be worth approximately US$169 million and represent around 15.6% of assets.

The latest filing

The Moonshot markup was already one of the largest movements in the fund’s portfolio last quarter. It added approximately HK$1.96 per share to NAV, but declines in other positions more than offset the increase. The fund reported NAV of US$4.954, or HK$38.83, per share as of 30 June.

This is relevant because Moonshot has moved from a small option in the portfolio to a position capable of affecting the reported NAV on its own. If K3 drives another valuation reset, the next Moonshot mark could be materially larger than the one reported this quarter.

What matters after launch

The first question is whether K3 is actually released as an open-weight model and under what license. GLM-5.2’s impact was amplified by its MIT license, downloadable weights and immediate availability across developer platforms. A strong closed API model would still matter for Moonshot, but it would not create the same open-weight adoption cycle.

The second is performance. K3 needs to hold up across coding, agent tasks, long-context reasoning and real-world frontend generation once broader testing begins. Individual Arena comparisons are useful early signals, but the model will need consistent performance across larger benchmark sets.

The third is economics. Pricing and inference speed could determine whether K3 becomes widely used even if its raw performance is strong. The current early feedback suggests output quality may be high, but latency could be a limitation due to the large parameter size.

Finally, TickerTrends Developer Activity and Kimi Consumer Usage should show whether the launch creates sustained adoption.

Risks

K3 may not match the early tester comparisons once it is broadly available. The reported specifications may also prove inaccurate, and Moonshot may release the model with restrictions that limit open-weight adoption.

Strong model performance may not translate into higher consumer usage or API revenue, particularly if inference is slow or expensive. The proposed US$30 billion to US$31.5 billion financing may also close at a lower valuation or not close at all.

For 133.HK, Moonshot remains one position within a broader closed-end portfolio. Even a meaningful Moonshot markup can be offset by declines elsewhere, as occurred last quarter.

Conclusion

Moonshot appears to be preparing a much larger agent-focused model at a time when open-weight models are rapidly closing the gap with the leading closed systems.

GLM-5.2 showed how quickly a strong Chinese open-weight release can move from limited awareness into global developer adoption. Early K3 outputs suggest Moonshot may have a credible chance of creating a similar moment, although the evidence remains too selective to reach that conclusion before launch.

133.HK provides the only meaningful listed exposure to that outcome. Its Moonshot position has already risen from 1.67% to 5.68% of assets and could move above 10% if marked to the May financing level.

The question is whether K3 becomes the next major open-weight model. If it does, the likely sequence is a re-acceleration in developer activity and usage, stronger API revenue, a higher Moonshot financing valuation and, eventually, a larger carrying value inside 133.HK.