Nitta Gelatin (TYO: 4977): The Play on the Global Collagen Boom

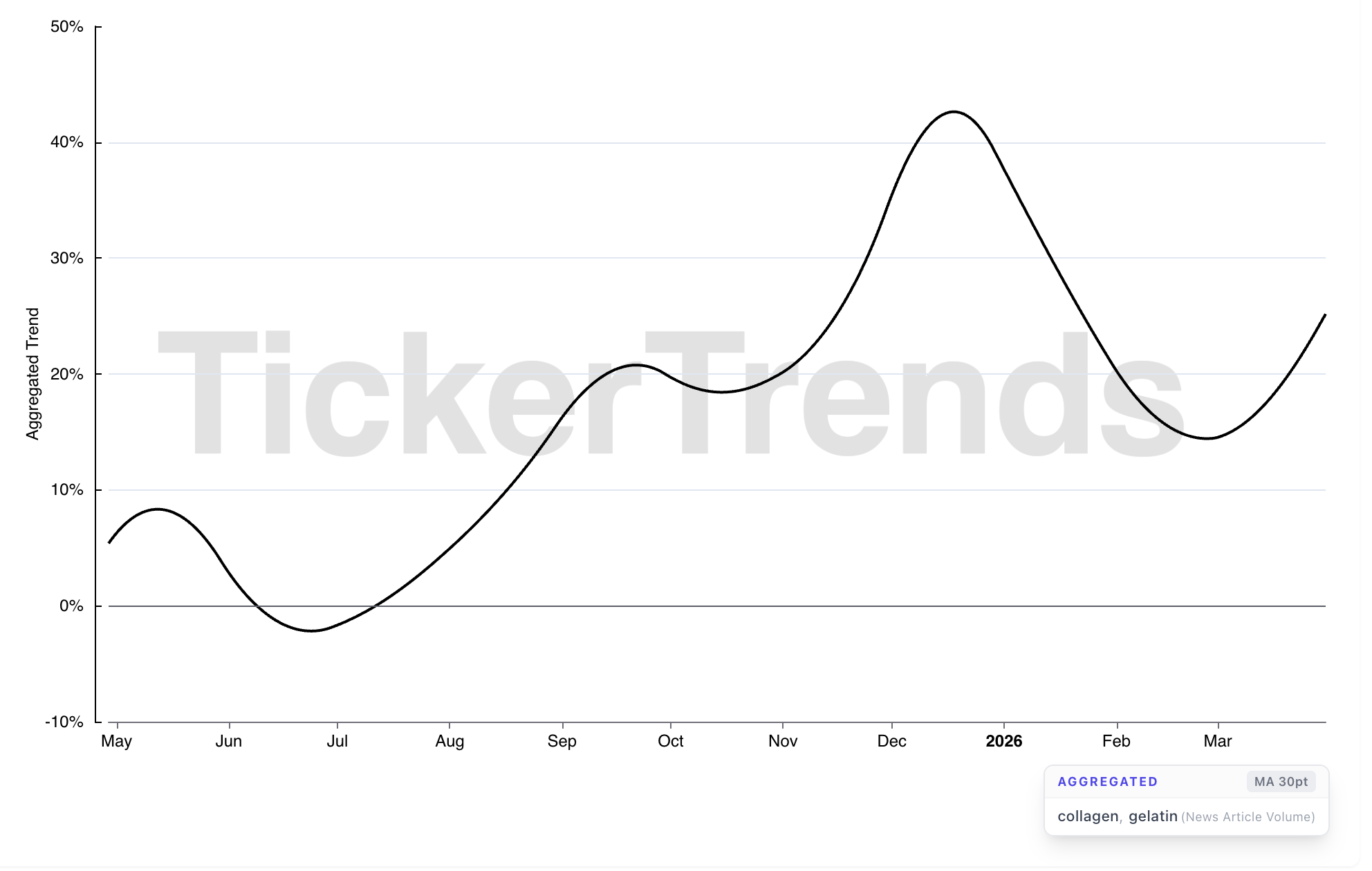

TickerTrends data shows accelerating collagen and gelatin demand driving potential upside to FY2026, with margin expansion and India-led supply positioning as key catalysts

TickerTrends data shows material acceleration in gelatin and collagen demand in North America, not yet fully reflected in Nitta Gelatin’s guidance.

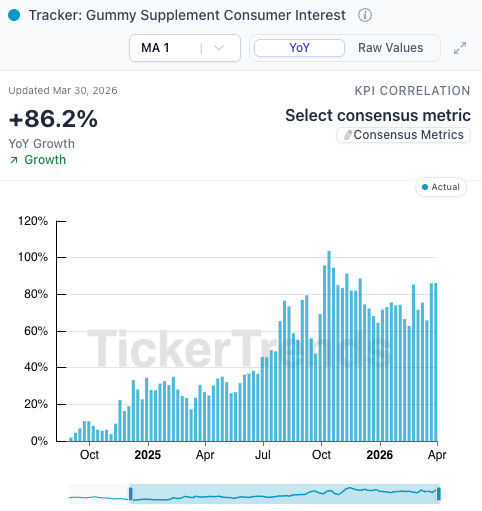

Nitta Gelatin (TYO: 4977) is one of the world’s largest gelatin and collagen peptide manufacturers, with operations across Japan, India, North America, China, and Vietnam. In the current peptide boom, collagen and more ancillary beneficiary products like gelatin are winners.

Key Data Signals

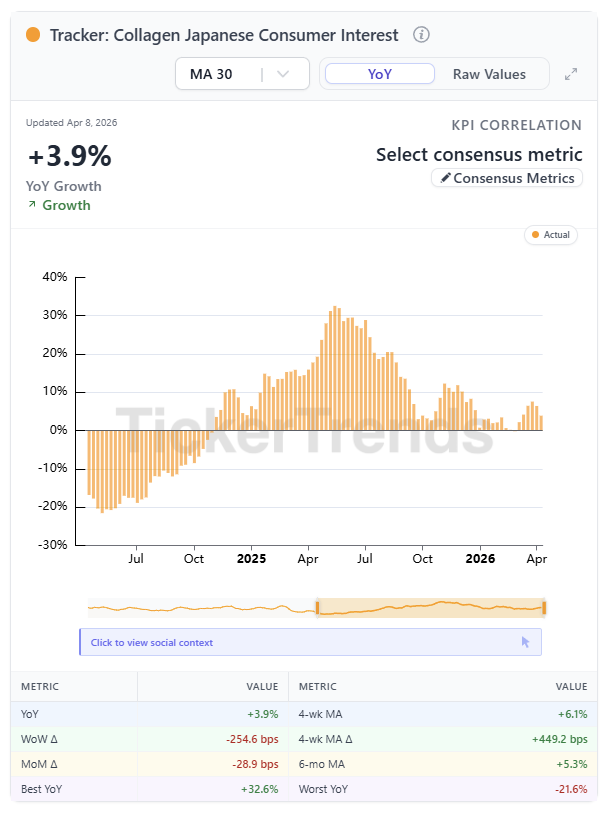

Japan (non-driver / drag) -

Gelatin: -5.3% YoY, no recovery signal

Collagen: +3.9% YoY, stable but not accelerating

Consistent with reported weakness. No near-term inflection.

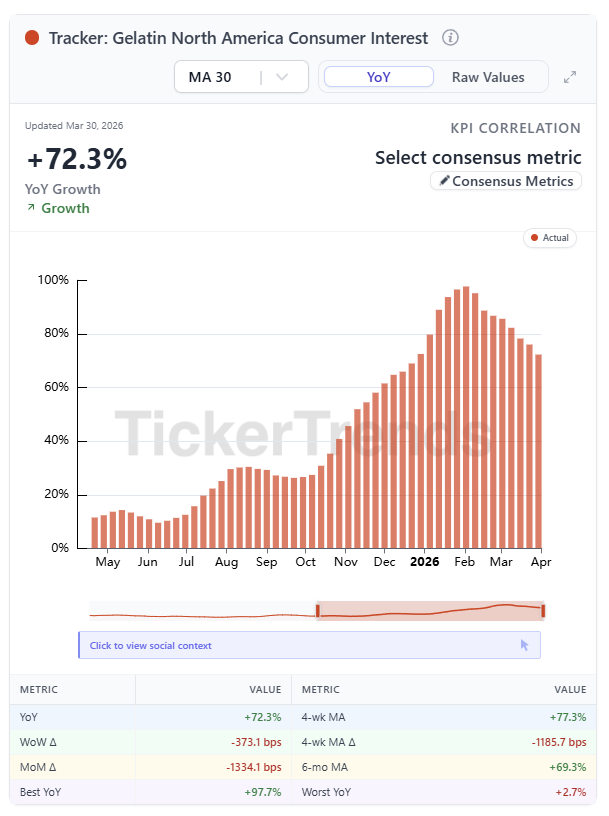

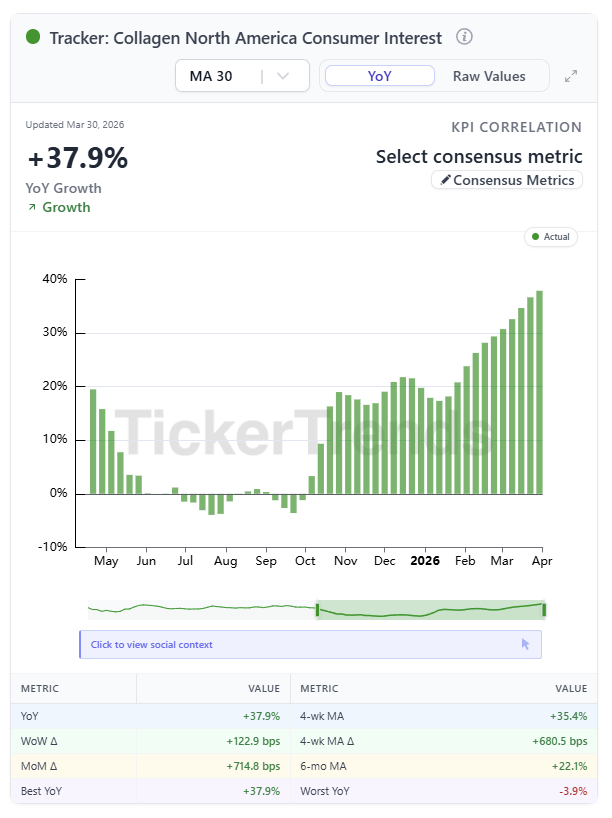

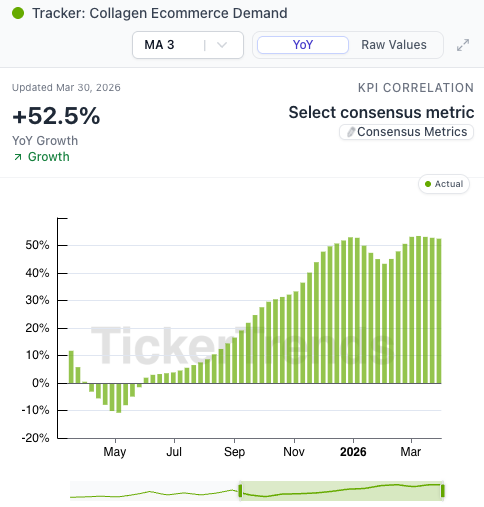

North America (core driver)

Gelatin: +72.3% YoY (sustained acceleration since mid-2025)

Collagen: +37.9% YoY with accelerating momentum

Management specifically called out North America demand in their latest earnings report with explicit mention of “demand for protein bars and similar applications”. The trend has significantly accelerated since that point. As top of funnel collagen demand rises, we think Nitta will continue to experience outperformance in this segment.

Financials

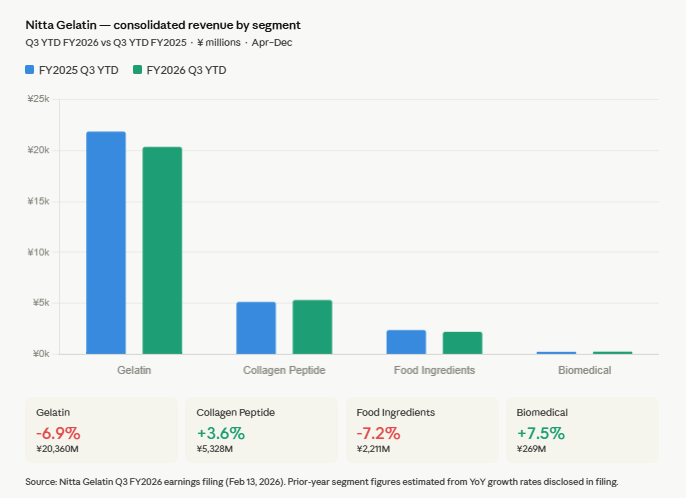

For the nine months ending December 2025 (Q3 YTD FY2026):

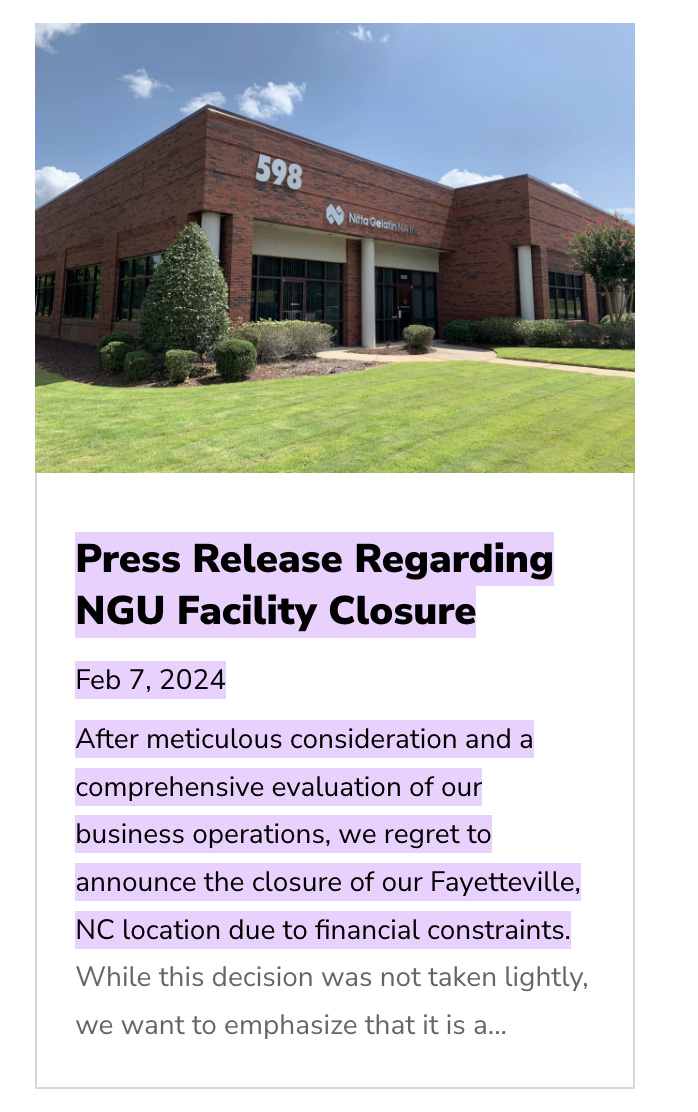

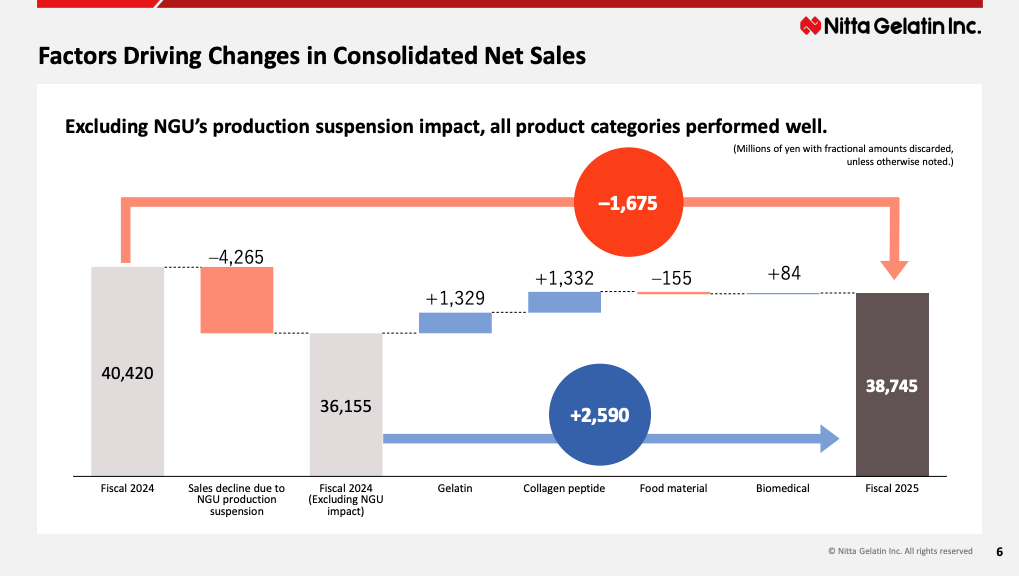

Gelatin: 20,360M yen, down 6.9% YoY (Due to NGU Closure)

Collagen Peptide: 5,328M yen, up 3.6% YoY

Food Ingredients: 2,211M yen, down 7.2% YoY

Biomedical: 269M yen, up 7.5% YoY

Total net sales: 28,170M yen, down 5.0% YoY

Revenue declined following the closure of NGU, but operating income increased 13.2% to 3,614M yen. Margin expansion was driven by improved North America profitability after exiting the loss-making U.S. manufacturing operation, with supply now shifted to exports from India.

FY2026 guidance calls for 40,000M yen in revenue (+3.2% YoY) and 4,000M yen in operating income. Current North America demand trends in gelatin and collagen suggest upside to this outlook if conversion into volume materializes. Additional upside would require stabilization in Japan, which remains a drag.

Within the portfolio, growth is more likely to be driven by collagen peptides than gelatin.

What to Watch

India capacity expansion

The company is scaling gelatin and collagen peptide capacity in India, now the primary supply hub. If capacity does not expand in line with demand, volume growth will be constrained despite strong end-market signals.

FY2026 close / Q4 results

Guidance was unchanged in the Q3 filing. Q4 results will be an indication of whether North America demand is translating into reported FY volume growth, or if tariffs and supply constraints are still limiting conversion.

Conclusion

The setup is centered on sustained strength in North America demand and an improved cost structure post-U.S. exit.

If current demand trends continue, the company is positioned for:

Continued growth in North America-driven segments

Further margin expansion through operating leverage

Mix shift toward higher-growth collagen peptide products

From a positioning standpoint, Nitta offers direct exposure to collagen and gelatin demand trends, with a cleaner and more focused profile than diversified ingredient peers.