What's Trending with TickerTrends #14

Your regular monitor for interesting social arbitrage ideas.

TickerTrend’s Monday Monitor is our overview of interesting social arbitrage event-driven trades and companies that could potentially benefit from these. We aim to find the best ideas driven by social arb. If you have any interesting ideas, feel free to contact us on X or join our Discord.

Enjoy!

Disclaimer. This newsletter is provided for informative purposes only. No significant due diligence has (yet) been performed on the names on this list. This overview does not constitute advice; always do your own due diligence.

Thanks for reading TickerTrends. Subscribe for free to receive new posts. Also, subscribe to our platform and support our work.

Important notice: We would like to continue to publish WTWT on a weekly basis, but we need a more critical mass. If you value this service, please like and hit the “share” button below. Thank you.

TickerTrends Research is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Earnings Recap:

You can get the transcripts for all earnings calls here: https://www.tickertrends.io/transcripts.

ARITZIA INC. ($ATZ.TO):

If you have not read our deep dive on Aritzia, check it out here: https://blog.tickertrends.io/p/atzto-everyday-luxury-defined-scaling?r=4ioql1&utm_campaign=post&utm_medium=web&showWelcomeOnShare=false.The stock is up ~38% since.

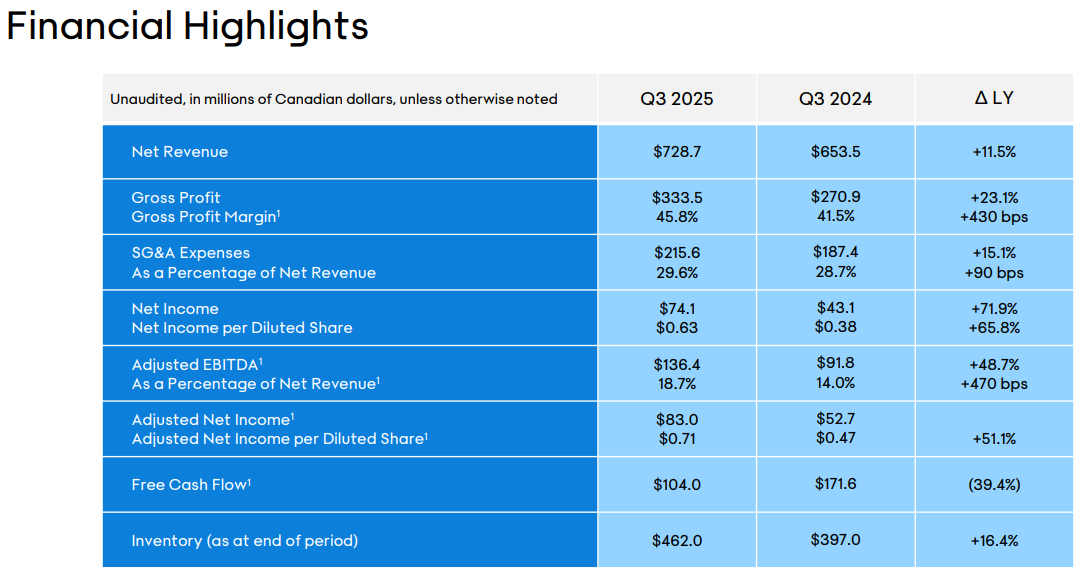

Aritzia delivered standout performance in its third quarter of fiscal 2025, showcasing robust growth and profitability. The company reported net revenue of $729 million, representing an 11.5% year-over-year increase. When adjusted for non-recurring events, such as last year’s Digital Archive Sale and the shift of the Vancouver Warehouse Sale to Q2 this year, normalized net revenue growth stood at an impressive 16%. This growth was largely fueled by the United States market, where normalized revenue surged 27%, reflecting the strong resonance of Aritzia’s everyday luxury offerings. In Canada, normalized net revenue grew by 5%, marking a meaningful improvement compared to prior trends.

Aritzia's eCommerce channel emerged as a key driver, with normalized revenue up 22%, accelerating for the third consecutive quarter. This was attributed to increased traffic in the U.S., bolstered by strategic digital marketing investments and a positive response to its Fall and Winter collections. The company also reported strong gains in its Retail channel, where normalized revenue grew by 13%. This growth was underpinned by the opening of 11 new boutiques and the repositioning of three flagship locations in the past year, including a highly anticipated SoHo store in New York City and a flagship on Michigan Avenue in Chicago. Both flagships exceeded expectations, serving not only as high-performing stores but also as brand-propelling marketing vehicles.

Gross profit grew 23% to $333 million, with gross profit margins expanding by 430 basis points to 45.8%, driven by improved initial markup (IMU), lower markdowns, and savings from operational efficiencies. Despite ongoing freight cost pressures, Aritzia's inventory optimization and spending initiatives supported this margin expansion. Selling, general, and administrative expenses increased in line with revenue, reflecting investments in digital marketing, infrastructure, and flagship launches.

Adjusted EBITDA rose significantly, up 49% year-over-year to $136 million, with the adjusted EBITDA margin expanding by 470 basis points to 18.7%. Net income for the quarter surged 72% to $74 million, or $0.63 per diluted share, compared to $0.38 per share in the prior year, reflecting a stronger operational performance and enhanced profitability.

Looking ahead, Aritzia provided optimistic guidance for the fourth quarter, forecasting net revenue of $830 to $850 million, representing growth of 22-25%, or 28-31% when normalized for an extra week in last year’s Q4. This momentum is expected to be driven by continued eCommerce acceleration, the impact of recent boutique openings, and strong comparable sales growth in existing stores. For fiscal 2025, the company raised its full-year revenue outlook to $2.67-$2.69 billion, up approximately 15% year-over-year.

Aritzia remains focused on advancing its three strategic growth levers: geographic expansion, eCommerce acceleration, and increasing brand awareness. The company plans to maintain its flagship-driven marketing approach, with another flagship store set to open in Manhattan’s Flatiron District in fiscal 2026. Digital initiatives, including the launch of an enhanced website and a highly anticipated mobile app, are also expected to drive further customer engagement and revenue growth. With a strong inventory position, record-breaking holiday sales, and a well-executed growth strategy, Aritzia is well-positioned for sustained long-term success.

Trends this week:

1. Nvidia Corp ($NVDA):

NVIDIA’s keynote at CES 2025, delivered by CEO Jensen Huang, showcased the company’s advancements in artificial intelligence, autonomous systems, and gaming technologies, while highlighting its vision for the future of AI-driven industries. Huang framed the evolution of robotics and autonomous vehicles (AVs) as a "three-body problem" and proposed a "three-computer solution" as the answer. This solution integrates three key components: NVIDIA DGX for AI training, NVIDIA AGX for edge inferencing, and Omniverse, which serves as a digital twin for simulation and refinement. The newly announced Cosmos platform, trained on 20 million hours of dynamic physical data, adds another layer to this ecosystem, enabling the creation of photorealistic, physically plausible synthetic data for use in robotics and AV development. This comprehensive system positions NVIDIA as a leader in connecting AI training, deployment, and continuous optimization across various industries.

The keynote also introduced the GB10 AI chip, a compact version of NVIDIA’s powerful GB200 platform, tailored for desktop AI applications. This chip will power Project DIGITS, a desktop AI computing system designed for developers and small enterprises.

By making high-performance AI more accessible, NVIDIA aims to expand its addressable market beyond large-scale enterprises to include smaller businesses and individual developers. Alongside its focus on AI, NVIDIA reinforced its dominance in gaming with the launch of the RTX 50 series of graphics cards, including the flagship RTX 5090, which delivers double the performance of its predecessor, the RTX 4090. These innovations ensure NVIDIA remains at the forefront of high-performance GPUs, a critical segment for both gaming and simulation.

In the automotive sector, NVIDIA highlighted its partnerships with Toyota, Continental, and Aurora, showcasing its role in powering advanced and autonomous driving systems. Huang described AVs as the “first multi-trillion-dollar robotics industry,” emphasizing the significant growth potential in this space. Similarly, the company unveiled tools such as the Isaac GROOT Blueprint software, designed to train humanoid robots using Apple Vision Pro, further cementing its position in robotics and industrial automation. These advancements underscore NVIDIA’s ability to provide end-to-end solutions across a range of transformative industries.

The announcements reflect NVIDIA’s strategy to expand its reach into multi-trillion-dollar markets like AVs, robotics, and industrial AI while maintaining a strong presence in gaming. Its diversified portfolio, from enterprise AI systems to consumer GPUs, mitigates risks associated with reliance on any single market. The Cosmos platform and its integration with Omniverse demonstrate NVIDIA’s ability to lead in the development of digital twins and simulation technologies, critical for future advancements in autonomous systems. While challenges such as macroeconomic uncertainty and competition from rivals like AMD and Google remain, NVIDIA’s consistent innovation and leadership in AI make it a compelling player in the rapidly evolving tech landscape.

NVIDIA’s keynote highlighted its focus on building comprehensive AI ecosystems to address the needs of industries ranging from robotics and AVs to gaming and enterprise AI. Its ability to balance cutting-edge innovation with practical applications ensures its continued leadership in the tech space. These advancements, paired with strong execution, position NVIDIA for sustained growth and reinforce its role as a key driver of the AI revolution.

2. Tesla Inc. ($TSLA):

Tesla’s launch of the redesigned Model Y in China marks a strategic effort to bolster its position in the increasingly competitive electric vehicle (EV) market, particularly against domestic rivals such as BYD, Xpeng, and Nio. The refreshed Model Y, starting at 263,500 Chinese yuan ($35,935), comes with several notable upgrades aimed at appealing to the local market. These include a revamped exterior design inspired by Tesla’s Cybertruck, improved aerodynamics, an extended range, faster acceleration, and a more refined interior with advanced features. The new Model Y will begin deliveries in China in March 2025, with Tesla targeting a segment that has seen fierce competition among SUVs.

The 2025 Model Y features significant changes, including a redesigned front with split headlights, a full-width LED light bar, and a revamped bumper. The rear showcases a striking full-width taillight design, while the side profile retains much of the original design. The interior maintains Tesla’s minimalist approach but adds a slightly larger 15.4-inch infotainment display and an additional 8-inch touchscreen for rear passengers, enabling entertainment and climate control. Upgraded seating, ventilated front seats, and ambient lighting enhance passenger comfort. Tesla has also introduced noise-reducing materials and retuned suspension for a quieter and smoother ride, emphasizing luxury and performance.

The performance upgrades are equally noteworthy. The rear-wheel drive model now accelerates from 0 to 100 km/h in 5.9 seconds, a full second faster than its predecessor, while the Long Range AWD version achieves the same in 4.3 seconds. The range has been extended, with the RWD model offering up to 593 kilometers (368 miles) on China’s CLTC cycle, and the Long Range AWD delivering 719 kilometers (446 miles). While these figures reflect China’s optimistic testing standards, they indicate a significant improvement over the previous generation.

Tesla is also emphasizing technological advancements with the new Model Y, including its Full Self-Driving suite, enhanced safety features, and over-the-air updates. The vehicle is designed to appeal to a broader audience, particularly in China, where localized features and a unique services ecosystem are critical to maintaining its market share. Additionally, Tesla is offering attractive incentives, such as a five-year, 0% interest financing plan, to boost demand.

This launch comes at a critical time for Tesla, which recently reported its first annual decline in deliveries for 2024, selling 1.79 million vehicles compared to 1.8 million in 2023. The EV market has faced headwinds, including reduced tax credits, limited charging infrastructure, and increasing competition. Tesla’s refreshed Model Y is a tactical response to these challenges, aiming to rejuvenate sales and reinforce its leadership in the EV segment. The redesign follows Tesla’s strategy of iterative innovation, akin to Apple’s approach with the iPhone, where incremental updates are preferred over entirely new product lines.

Investor sentiment remains cautiously optimistic, as the new Model Y provides a fresh focal point for Tesla’s 2025 lineup. With additional launches, including a rumored affordable EV, and the introduction of cheaper variants, Tesla is poised to address broader market needs. The company’s ability to maintain its dominance in key markets like China while navigating an evolving EV landscape will be critical for its long-term growth and stock performance. The Model Y’s refresh reflects Tesla’s commitment to innovation, market responsiveness, and its ongoing pursuit of excellence in electric mobility.

3. FuboTv Inc. ($FUBO):

$FUBO stock was up 259.86% this week. If you missed our article on it check it out here:

Disney’s decision to merge its Hulu Live + TV service with Fubo represents a significant development in the competitive streaming landscape, creating the second-largest virtual multichannel video programming distributor (vMVPD) in North America with over 6.2 million subscribers and $6 billion in revenue. Disney will own 70% of the combined entity, while Fubo retains the remaining 30% and operational leadership under CEO David Gandler. This strategic move aims to consolidate resources, broaden consumer options, and strengthen both companies’ positions in the evolving streaming market.

The merger will preserve Hulu Live + TV and Fubo as separate offerings, but the combined entity will also provide new bundled packages tailored to consumers’ varied interests. Fubo will focus on sports and news, leveraging its new carriage agreements with Disney to include ESPN networks, ESPN+, and other Disney channels in its offerings. These agreements enable Fubo to create a specialized sports and broadcast service while maintaining Hulu Live + TV’s position as an entertainment-centric service. The combination provides both entities with the scale and leverage needed to negotiate content rights and drive revenue growth through targeted programmatic advertising and enhanced subscription options.

This merger also resolves the litigation between Fubo and Disney, Fox, and Warner Bros. Discovery over the stalled launch of Venu Sports, a sports-streaming joint venture. As part of the settlement, Disney, Fox, and Warner Bros. agreed to pay Fubo $220 million, with Disney providing an additional $145 million term loan in 2026.

Analysts have offered mixed reactions to the deal. While some, such as Macquarie’s Tim Nollen, view it as a financially modest but strategically positive step for Disney to consolidate its distribution business and scale its streaming operations, others, like Moffett Nathanson, argue that it further complicates Disney’s streaming strategy. The merged entity now exists alongside Disney+, ESPN+, Hulu, and the forthcoming ESPN Flagship direct-to-consumer service, potentially creating a fragmented ecosystem. However, this fragmentation may also represent Disney’s effort to cover all market segments, particularly in sports streaming, where competition for rights remains fierce.

For Fubo, the merger is a transformative opportunity. The partnership provides scale, resolves critical legal challenges, and positions the company to capitalize on its sports-centric focus. Analysts predict accelerated subscriber growth and revenue increases, with Fubo expected to add 500,000 to 1 million subscribers annually over the next four years. This projection, coupled with the resolution of its financial and operational hurdles, has led to optimistic stock price revisions, including Wedbush’s revised target of $6.40, up from $3.00.

The broader implications of this merger reflect the rapidly shifting dynamics of the streaming and pay-TV industries. As more consumers cut traditional cable subscriptions, vMVPDs like Hulu Live + TV and Fubo face growing pressure to deliver competitive offerings while managing rising content costs. The merger allows the combined entity to better navigate this challenging environment, offering consumers expanded options and potentially reshaping the market for live TV and sports streaming. However, rising subscription costs and market fragmentation remain significant challenges, as analysts predict continued price hikes across all streaming services.

Overall, the Disney-Fubo merger signals a strategic pivot for both companies as they adapt to the changing media landscape. For Disney, it streamlines its direct-to-consumer operations while expanding its reach in sports streaming. For Fubo, it represents a chance to redefine itself as a leading sports-focused streaming service with the backing of one of the world’s largest entertainment companies. The deal sets the stage for further consolidation and innovation in the streaming industry, as companies vie for dominance in an increasingly competitive market.

4. Walt Disney Co ($DIS):

Disney’s highly successful Moana 2 has hit an unexpected hurdle during awards season as the company faces a lawsuit over alleged copyright infringement. Animator Buck Woodall has filed a lawsuit in California federal court claiming Disney stole elements from his 2003 screenplay, Bucky, and used them in both Moana films. Woodall seeks damages equivalent to 2.5% of Moana’s gross revenue, amounting to $10 billion. The case comes after the court ruled in November that it was too late for Woodall to file a copyright lawsuit for the original Moana but allowed him to initiate legal action against Moana 2 due to its recent release.

Woodall alleges striking similarities between his screenplay and Disney’s films, including themes of Polynesian cultural traditions, a teenager defying their parents to save their home, spirits manifesting as animals, and a demigod with a hook and tattoos. Specific narrative overlaps include a journey starting with a turtle, a symbolic necklace, a giant creature hidden within a mountain, and characters navigating a whirlpool-like ocean portal. The lawsuit also extends to Moana 2, citing similarities such as a mission to break a curse and a search for an ancient island.

The origins of the lawsuit trace back to 2003, when Woodall submitted his Bucky screenplay, a trailer, and related materials to Jenny Marchick, then the director of development at Mandeville Films, which had a first-look deal with Disney. Woodall claims Marchick expressed interest and requested further materials, such as character designs and storyboards. Although the court acknowledged that Disney personnel may have had access to Bucky materials, Disney has firmly denied the allegations. Director Ron Clements submitted a declaration stating that Moana was not inspired by or based on Woodall’s work, asserting that he first learned of Bucky when the lawsuit was filed.

To defend its position, Disney has provided extensive documentation regarding the development of Moana, including story ideas, research materials, and travel journals. The company contends that Moana was an original creation rooted in extensive research on Polynesian culture and mythology.

The timing of the lawsuit could impact the film’s awards season trajectory, with Moana 2 already shortlisted for an Academy Award for Best Original Song and positioned as a strong contender for Best Animated Feature. The controversy may discourage nominations, as the Academy and other awards organizations might aim to avoid potential backlash. While Moana 2 lost the Golden Globe for Best Animated Feature to Flow, the lawsuit adds another layer of complexity to its awards campaign.

If the court rules in favor of Woodall, the future of the Moana franchise could be at risk. While Disney could attempt to settle with Woodall or integrate him into future projects, the allegations might cast a shadow over the planned live-action adaptation and any potential sequels. The lawsuit underscores the broader challenges of originality and intellectual property in the entertainment industry, particularly for a company as prominent as Disney.

5. Wendy’s Co ($WEN):

Wendy’s has kicked off 2025 with an exciting new promotion to help customers save money while enjoying some of their most popular menu items. The fast food giant has launched a limited-time 2 for $7 deal, available until March 2, allowing customers to mix and match two items from a selection of fan favorites. The options include the Spicy Chicken Sandwich, Classic Chicken Sandwich, Dave’s Single cheeseburger, and a 10-piece order of chicken nuggets (available in both crispy and spicy varieties). Customers can also choose two of the same item if preferred. The promotion can be redeemed in-store or through the Wendy’s app under the “Meal Deals” section.

In addition to this offer, Wendy’s is celebrating 25 years since the turn of the century with another eye-catching deal: Dave’s Single cheeseburger for just 25 cents. This promotion is valid from January 9 through January 13 and requires a minimum order of $20 via Grubhub for delivery or pickup from participating locations. Wendy’s is also continuing its popular Frosty Key Tag promotion, which allows customers to receive free Junior Frostys with any purchase for the entire year for just $3. These tags are available for purchase in Wendy’s restaurants, through the app, or on the Dave Thomas Foundation for Adoption website, which supports children in foster care.

The 2 for $7 deal follows a series of promotions Wendy’s has introduced to help customers save, including their December "Bow-GO" campaign offering buy-one-get-one-free deals on select items and the price drop of their Spicy Chicken Sandwich to $4 in late 2024. With these offers, Wendy’s is helping customers stick to New Year’s resolutions to save money while enjoying flavorful meals.

The promotion also arrives amidst increased competition in the fast food value space. McDonald’s recently launched its new McValue Menu featuring $5 meal deals and in-app discounts, while Taco Bell is introducing Luxe Cravings Boxes priced at $5, $7, and $9 later in January. Wendy’s, however, is carving its niche by offering affordable options without compromising quality. With its customizable 2 for $7 deal and additional savings opportunities like the Frosty Key Tag, Wendy’s is positioning itself as a go-to choice for customers seeking both value and variety. These promotions underscore the brand’s commitment to delivering satisfying meals that are both affordable and indulgent, making it easier than ever for customers to enjoy their favorites without breaking the bank.

6. Advanced Micro Devices Inc ($AMD):

Advanced Micro Devices (AMD) has faced challenges over the past three years, with its shares declining 5% even as the PHLX Semiconductor Sector index rose 36%. The company’s reliance on the weakening personal computer (PC) and gaming markets, coupled with its struggles to compete against Nvidia in the artificial intelligence (AI) data center space, has weighed heavily on its performance. However, AMD is positioning itself for a turnaround driven by a recovering PC market, advancements in its data center business, and renewed opportunities in the gaming sector.

The PC market, which saw significant declines in 2022 and 2023, stabilized in 2024 and is projected to grow by 4.3% in 2025, driven by increased demand for commercial PCs and the transition to AI-capable machines. The market is expected to expand at an annual rate of 1.4% through 2028, with AI-capable PCs projected to account for 60% of the market by 2027. AMD is well-positioned to capitalize on this growth, with Dell Technologies now integrating AMD’s processors into its commercial PCs for the first time. Additionally, AMD’s AI-enabled CPUs will power over 100 commercial PC platforms in 2025. These developments come alongside AMD’s ongoing gains in client CPU market share, which grew from 19.4% in Q3 2023 to 23.9% in Q3 2024, contributing to a 29% year-over-year increase in revenue from the segment.

In the data center business, AMD reported a remarkable 122% year-over-year revenue increase in Q3 2024, driven by robust demand for its graphics cards and expanding server CPU market share. AMD anticipates the total addressable market (TAM) for data center AI chips to grow at an annual rate of 60% through 2028, reaching $500 billion in revenue. While Nvidia dominates this space, AMD’s plan to release new data center GPUs annually and its focus on enhancing supply chain efficiency positions the company to gain a foothold in this lucrative market. Even capturing 10% of the data center GPU market by 2028 could translate into $50 billion in revenue for AMD, a tenfold increase from its 2024 projections of $5 billion in data center GPU revenue.

The gaming sector, though a headwind in 2024, offers long-term potential with the anticipated launch of next-generation gaming consoles from Microsoft and Sony within the next three years. AMD supplies the semi-custom chips powering these consoles, and it is expected to continue as the primary supplier for future iterations. This development could reverse the 69% year-over-year decline in AMD’s gaming revenue reported in Q3 2024, potentially rejuvenating the segment.

Despite its promising outlook, AMD has faced skepticism from analysts. Goldman Sachs recently downgraded the stock from Buy to Neutral, citing a modest demand outlook for PCs, servers, and data center GPUs, as well as increased competition. The price target was lowered to $129 from $175. AMD’s underperformance relative to peers like Nvidia, which has solidified its dominance in the AI space, reflects the broader divergence within the semiconductor sector, where companies heavily tied to AI have outperformed those more reliant on traditional markets. However, AMD’s focus on AI-enabled CPUs, robust data center ambitions, and strategic positioning in the gaming market could help it regain investor confidence.

In the GPU space, AMD is pursuing a different strategy with its RDNA 4 architecture, shifting away from the ultra-high-end market to focus on delivering strong price-to-performance ratios in the mainstream segment. The upcoming Radeon RX 9070 XT and RX 9070 GPUs are expected to offer competitive performance at accessible price points, with the RX 9070 XT positioned as a rival to Nvidia’s midrange GPUs. The RDNA 4 lineup emphasizes efficiency and affordability, catering to gamers seeking high performance without the premium price tag.

Early benchmarks suggest that the RX 9070 XT delivers impressive performance, rivaling higher-end GPUs from previous generations. The GPUs, which are set to begin preorders on January 23, are anticipated to disrupt the mainstream market, further solidifying AMD’s position in gaming hardware.

With consensus estimates projecting AMD’s earnings to grow at an annual rate of 45% over the next few years, the company is poised for a resurgence. Its strategic moves in the PC, data center, and gaming markets, combined with its focus on innovation and competitive pricing, position AMD to capitalize on emerging opportunities and drive long-term growth. While challenges remain, AMD’s roadmap suggests a brighter future, offering potential for the stock to rebound and deliver significant value to investors.

7. Sharkninja ($SN):

Read our deep dive on SharkNinja here if you haven’t already:

Ninja is set to redefine the home ice cream-making experience with the upcoming launch of its Ninja Creami Swirl, blending the beloved features of the original Creami with the addition of a soft-serve dispenser. Though the company has yet to make an official announcement, social media is abuzz with sneak peeks from influencers showcasing the machine’s capabilities. Building on the success of the Ninja Creami and Creami Deluxe, this new model promises to elevate frozen dessert preparation by combining the versatility of its predecessors with the ability to create soft-serve ice cream. The Ninja Swirl’s functionality allows users to process frozen bases into soft-serve texture, using a dispensing arm to create swirls directly into cones or cups.

The Creami Swirl includes a new "Creamifit" setting, specifically designed for protein-based recipes that have gained popularity within fitness communities. Users can also make frozen yogurt, sorbet, gelato, and other treats with its multiple settings. The machine appears larger than previous Creami models, a trade-off for the added soft-serve functionality. Influencers who have previewed the appliance report that it can produce up to four or five servings of soft-serve from a single preparation. Early reviews highlight its ease of use and the impressive texture of the desserts, making it a contender for the must-have kitchen gadget of 2025.

Ninja has yet to disclose pricing or an official release date, though the Swirl is expected to launch in February. Fans can already sign up for a waitlist on Ninja’s website to receive updates. This new addition to the Ninja lineup capitalizes on the popularity of the original Creami and the fitness-driven #creamifit trend, which has inspired countless recipes and social media content dedicated to low-calorie, high-protein frozen desserts. With its ability to create both scoopable and soft-serve ice cream, the Creami Swirl offers something for everyone, whether they prefer traditional frozen treats or health-conscious alternatives.

As anticipation builds, the Creami Swirl is expected to follow in the footsteps of other successful Ninja appliances, such as the Creami Deluxe and the recently launched Slushi machine, both of which garnered widespread acclaim for their innovative designs and functionality. With the Creami Swirl, Ninja continues its legacy of delivering high-quality, affordable kitchen gadgets that resonate with consumers seeking both convenience and creativity in the kitchen. While full details remain under wraps, the buzz surrounding the Creami Swirl suggests it will be a game-changer for home dessert enthusiasts, offering a professional soft-serve experience right on the countertop.

Thanks for reading What’s Trending with TickerTrends. Subscribe for free to receive new posts and support our work.

TickerTrends Research is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.